How to Start a Blog Without These 5 Costly Beginner Errors

Starting a blog feels like launching into uncharted territory. You’re ready to share your expertise with the world, but one wrong move can waste months of effort and hundreds of dollars. This guide is for aspiring bloggers and business owners who want to build a successful blog from day one. We’ll walk through how to […]

What is the difference between SIP and lump-sum investment?

SIP (Systematic Investment Plan) and lump-sum investment are two popular approaches to investing in mutual funds. Here is the key difference between the two:SIP (Systematic Investment Plan):- In SIP, investors can invest a fixed amount regularly at predefined intervals, such as monthly or quarterly.Read more

SIP (Systematic Investment Plan) and lump-sum investment are two popular approaches to investing in mutual funds. Here is the key difference between the two:

SIP (Systematic Investment Plan):

– In SIP, investors can invest a fixed amount regularly at predefined intervals, such as monthly or quarterly.

– SIP helps in rupee cost averaging, spreading the investment over time, reducing the impact of market volatility.

– It instills financial discipline as investors commit to regular investments regardless of market conditions.

– Ideal for investors looking to invest small amounts periodically and benefit from the power of compounding over the long term.

– Suited for individuals who want to invest but may not have a lump sum amount to invest upfront.

Lump-Sum Investment:

– Lump-sum investment involves investing a significant amount of money in one go.

– The investor puts all the money into the market at once, benefiting if the market goes up immediately.

– There is no rupee cost averaging, so the investor faces the full impact of market volatility.

– Well-suited for investors with a large sum of money available for investment and who have analyzed the market for potential investment opportunities.

– Can be more beneficial in certain scenarios like market lows or when there’s a substantial opportunity for growth.

Key Considerations:

– SIP is a preferred choice for retail investors with regular income and lower risk appetite.

– Lump-sum investment is more suitable for investors with a higher risk appetite and a clear understanding of market conditions

See lessHow much risk is too much when investing?

When it comes to investing, determining how much risk is too much is a crucial consideration that varies depending on individual factors such as financial goals, time horizon, and risk tolerance. Here are some important points to help you gauge the right level of risk for your investment strategy: 1Read more

When it comes to investing, determining how much risk is too much is a crucial consideration that varies depending on individual factors such as financial goals, time horizon, and risk tolerance. Here are some important points to help you gauge the right level of risk for your investment strategy:

1. Understand Your Risk Tolerance: It’s essential to assess your comfort level with risk. Are you able to sleep soundly at night despite market fluctuations, or does the thought of potential losses keep you up? Knowing yourself in this aspect is key.

2. Consider Your Investment Goals: The amount of risk you can take on should align with your financial objectives. Short-term goals like buying a house may require more conservative, lower-risk investments, while long-term goals like retirement savings may allow for more risk-taking.

3. Diversification: Spreading your investments across different asset classes can help mitigate risk. Diversification can reduce the impact of a negative event on any single investment.

4. Time Horizon: Generally, the longer your investment horizon, the more risk you can afford to take. Younger investors with decades until retirement can typically withstand more risk than those nearing retirement.

5. Stay Informed: Keep yourself updated on market trends, economic indicators, and investment opportunities. Understanding what you’re investing in can help you make informed decisions and manage risk better.

6. Professional Advice: If you’re unsure about how much risk is appropriate for your situation, consider seeking advice from a financial

See lessShould I invest in stocks or mutual funds first?

When deciding whether to invest in stocks or mutual funds first, there are several factors to consider to make an informed decision that aligns with your financial goals, risk tolerance, and investment timeframe: 1. Diversification: Mutual funds inherently offer diversification by pooling money fromRead more

When deciding whether to invest in stocks or mutual funds first, there are several factors to consider to make an informed decision that aligns with your financial goals, risk tolerance, and investment timeframe:

1. Diversification: Mutual funds inherently offer diversification by pooling money from multiple investors to invest in a variety of securities, reducing individual stock risk.

2. Risk Management: Stocks are generally riskier than mutual funds due to their individual company exposure. Mutual funds, on the other hand, can spread the risk across a portfolio of assets.

3. Expert Management: Mutual funds are managed by professionals who make investment decisions on behalf of investors. This can be beneficial for those who lack the time or expertise to research and manage individual stocks.

4. Costs and Fees: Mutual funds often have higher fees compared to investing directly in stocks. Be mindful of expense ratios, loads, and other costs associated with mutual funds.

5. Ease of Entry: Investing in mutual funds can be simpler for beginners as it requires less research and monitoring compared to picking individual stocks.

6. Potential Returns: While individual stocks can offer higher return potential, they come with greater volatility. Mutual funds tend to provide more stable returns over the long term.

7. Tax Implications: Mutual funds may distribute capital gains that could lead to tax liabilities, whereas individual stock investors can control the timing of their gains and losses.

In conclusion, determining whether to invest in stocks or mutual funds first depends on your financial

See lessWhy choose an AC Maintenance Company in Dubai for regular servicing?

Regular servicing of your AC system by a professional maintenance company in Dubai is crucial for several reasons:Hidden User Pain Points: 1. Increased Energy Efficiency: A well-maintained AC system operates more efficiently, helping you save on energy costs. 2. Enhanced Indoor Air Quality: RegularRead more

Regular servicing of your AC system by a professional maintenance company in Dubai is crucial for several reasons:

Hidden User Pain Points:

1. Increased Energy Efficiency: A well-maintained AC system operates more efficiently, helping you save on energy costs.

2. Enhanced Indoor Air Quality: Regular servicing ensures that your AC system is clean and functioning properly, reducing the risk of allergens and pollutants circulating in your home.

3. Prevention of Breakdowns: Routine maintenance can catch small issues before they escalate into major breakdowns, saving you from unexpected repair costs.

Source Awareness:

– The U.S. Department of Energy recommends regular AC maintenance to ensure optimal performance and longevity of your system.

– The American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) underscores the importance of periodic maintenance to maintain indoor air quality and comfort.

By choosing a professional AC maintenance company in Dubai, you benefit from their expertise, tools, and resources to keep your AC system in top condition. From cleaning the coils and filters to checking refrigerant levels and electrical connections, a maintenance company can address key aspects that are essential for your AC’s performance and durability.

In addition, professional maintenance can also help maintain your manufacturer’s warranty and extend the lifespan of your AC system, providing you with peace of mind and comfort throughout the year.

Hope this helps—feel free to share any challenges you’ve faced with AC maintenance or ask for more personalized tips on choosing a maintenance company in

See lessWhy is Limousine Chauffeur Service in Riyadh ideal for luxury travel?

Limousine chauffeur service in Riyadh is ideal for luxury travel for several reasons:Exclusivity and sophistication: Limousines exude luxury and elegance, making them the perfect choice for those looking to indulge in a first-class travel experience.Professional chauffeurs: Limousine chauffeur serviRead more

Limousine chauffeur service in Riyadh is ideal for luxury travel for several reasons:

Exclusivity and sophistication: Limousines exude luxury and elegance, making them the perfect choice for those looking to indulge in a first-class travel experience.

Professional chauffeurs: Limousine chauffeur services in Riyadh typically employ highly trained and professional drivers who provide top-notch customer service, ensuring a smooth and enjoyable journey.

Comfort and convenience: Limousines offer spacious interiors, plush seating, and amenities like Wi-Fi, entertainment systems, and refreshments, enhancing the overall travel experience.

Safety and security: With experienced chauffeurs behind the wheel, passengers can feel safe and secure throughout their journey, especially important for luxury travelers valuing peace of mind.

Time efficiency: Limousine services often include personalized itinerary planning and efficient routes, helping clients optimize their time and make the most of their travel experience.

Image and prestige: Arriving in a chauffeur-driven limousine provides a statement of status and sophistication, which can be particularly appealing for special occasions or business-related travel.

To access these benefits and elevate your travel experience, opting for a limousine chauffeur service in Riyadh is a wise choice for luxury travelers seeking unparalleled comfort, style, and service.

Hope this helps—feel free to add your experience or ask a follow-up.

See lessWhat is the best investment for beginners in India?

Investing for beginners in India can seem daunting, but with the right approach, you can start building wealth steadily. Here are some of the best investment options tailored for beginners in India: 1. Mutual Funds: Considered one of the safest and beginner-friendly investment options. Mutual fundsRead more

Investing for beginners in India can seem daunting, but with the right approach, you can start building wealth steadily. Here are some of the best investment options tailored for beginners in India:

1. Mutual Funds: Considered one of the safest and beginner-friendly investment options. Mutual funds pool money from multiple investors to invest in stocks, bonds, or other assets. They are managed by professional fund managers.

2. Public Provident Fund (PPF): A popular long-term investment scheme with a lock-in period of 15 years, PPF offers tax benefits and a guaranteed return. It’s a low-risk investment ideal for retirement planning.

3. SIP (Systematic Investment Plan): SIP is a convenient way to invest in mutual funds regularly. You can start with a small amount and invest periodically, reducing the impact of market volatility.

4. Stock Market: While it involves risk, investing in the stock market can offer high returns. Beginners can start with blue-chip stocks or take the help of a financial advisor.

5. Recurring Deposits: RDs are offered by banks, allowing investors to deposit a fixed amount monthly. The interest rates are usually higher than savings accounts.

6. Gold: Indians traditionally value gold as an investment. You can invest in physical gold, gold ETFs, or sovereign gold bonds.

7. National Pension System (NPS): NPS is a voluntary, long-term retirement savings scheme designed to enable systematic

See lessHow can I save money on groceries each month?

Saving money on groceries each month is a common goal for many people looking to trim their expenses. Here are some expert tips to help you achieve this without compromising on the quality of your meals:1. Plan your meals and create a shopping list:- Plan your meals for the week before heading to thRead more

Saving money on groceries each month is a common goal for many people looking to trim their expenses. Here are some expert tips to help you achieve this without compromising on the quality of your meals:

1. Plan your meals and create a shopping list:

– Plan your meals for the week before heading to the store.

– Create a detailed shopping list based on your meal plan to avoid impulse purchases.

2. Shop with a budget in mind:

– Set a budget for your groceries and stick to it.

– Consider using cash instead of cards to prevent overspending.

3. Take advantage of sales and discounts:

– Look for coupons, discounts, and special offers from your local grocery stores.

– Consider buying non-perishable items in bulk when they are on sale.

4. Buy in-season produce:

– In-season fruits and vegetables are usually cheaper and fresher.

– Check for local farmers’ markets for affordable options.

5. Cook and eat at home:

– Eating out can be expensive compared to cooking meals at home.

– Prepare large batches of meals and freeze them for later to save time and money.

6. Avoid buying convenience foods:

– Pre-packaged and processed foods tend to be more expensive.

– Opt for whole foods and prepare them yourself to save money.

7. Compare prices and consider store brands:

– Compare prices between different brands and opt for store

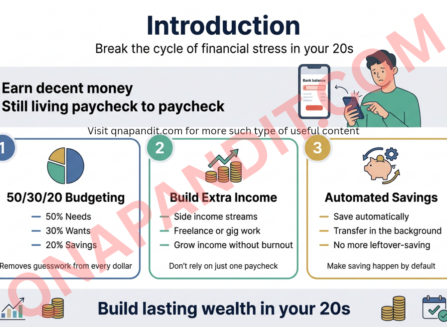

See lessHow much should I save for retirement in my 20s?

Saving for retirement in your 20s is a smart financial move that can set you up for a comfortable future. Here's a guide on how much you should save: 1. Start Early: Time is your biggest asset when saving for retirement due to the power of compounding interest. The earlier you start, the less you'llRead more

Saving for retirement in your 20s is a smart financial move that can set you up for a comfortable future. Here’s a guide on how much you should save:

1. Start Early: Time is your biggest asset when saving for retirement due to the power of compounding interest. The earlier you start, the less you’ll have to save each month to reach your goal.

2. Set a Target: Financial experts often recommend saving between 10% to 15% of your income for retirement. However, everyone’s situation is unique so adjust this percentage based on your income, expenses, and retirement goals.

3. Consider Matching Contributions: If your employer offers a retirement savings plan like a 401(k) with a matching contribution, try to contribute enough to get the full match. It’s essentially free money and boosts your retirement savings significantly.

4. Use Retirement Calculators: Online retirement calculators can help you estimate how much you should save based on factors like your age, income, current savings, and retirement age. This can give you a clearer picture of your retirement savings goal.

5. Increase Savings with Income Growth: As your income grows throughout your career, aim to increase your retirement savings contributions. This will help you stay on track to reach your retirement savings goal.

6. Monitor and Adjust: Regularly review your retirement savings progress and be prepared to adjust your contributions if needed. Life circumstances change, so it’s important to stay flexible with your savings

See lessWhat are the common budgeting mistakes to avoid?

Common budgeting mistakes to avoid include: 1. Not Creating a Detailed Budget: Failing to establish a comprehensive budget can lead to overspending, missed savings opportunities, and financial insecurity. 2. Underestimating Expenses: Many people only consider fixed expenses like rent or mortgage payRead more

Common budgeting mistakes to avoid include:

1. Not Creating a Detailed Budget: Failing to establish a comprehensive budget can lead to overspending, missed savings opportunities, and financial insecurity.

2. Underestimating Expenses: Many people only consider fixed expenses like rent or mortgage payments, but forget about irregular expenses like car repairs or medical bills. It’s crucial to account for all potential expenses.

3. Ignoring Emergency Funds: Not setting aside money for unexpected emergencies can derail your financial goals when unforeseen expenses arise.

4. Failing to Track Spending: Without monitoring your expenses regularly, it’s easy to lose control of your budget. Tracking your spending helps identify areas where you can cut back or save more.

5. Relying on Credit Cards: Depending on credit cards to cover budget shortfalls can lead to high-interest debt that becomes difficult to pay off, creating a cycle of financial stress.

6. Overlooking Small Expenses: While small purchases may seem insignificant, they can add up over time and sabotage your budget. Being mindful of even minor expenses is essential for staying on track.

7. Not Reviewing and Adjusting Your Budget: Circumstances change, so it’s essential to regularly review your budget and make necessary adjustments to ensure it aligns with your financial goals.

8. Forgetting Long-term Financial Planning: Focusing solely on immediate financial needs without considering long-term goals like retirement savings or investments can hinder your overall financial well-being.

It’s

See lessHow to budget for irregular income?

Budgeting for irregular income can be challenging, but with the right strategies, you can effectively manage your finances. Here are some expert tips to help you budget for irregular income: 1. Calculate Your Average Monthly Income:- Review your income from the past year or more to determine an averRead more

Budgeting for irregular income can be challenging, but with the right strategies, you can effectively manage your finances. Here are some expert tips to help you budget for irregular income:

1. Calculate Your Average Monthly Income:

– Review your income from the past year or more to determine an average monthly income. This will give you a baseline to work with.

2. Create a Bare-Bones Budget:

– Identify essential expenses like housing, utilities, groceries, and transportation. Allocate funds to cover these necessities first.

3. Build an Emergency Fund:

– Set aside money from your irregular income to create an emergency fund that can cover unexpected expenses or income gaps.

4. Prioritize Savings Goals:

– Determine your financial goals such as debt repayment, retirement savings, or a major purchase. Allocate a portion of your income to each goal.

5. Use a Zero-Sum Budget Approach:

– Give every dollar a job by assigning specific categories for spending, saving, and investing. Adjust your budget as your income varies.

6. Track Your Spending:

– Keep a close eye on your expenses to ensure you’re staying within your budget. Use budgeting tools or apps to help you track your financial transactions.

7. Adjust Your Budget Regularly:

– Since your income fluctuates, it’s important to review and adjust your budget on a regular basis. Be flexible and adaptable to changes in your financial situation.

8

See less