You’ve got money to manage, but you’re stuck on a big question: Should you build an emergency fund or start investing first?

This decision stumps many people, especially young adults and new earners who want to grow wealth but also need financial security. You know investing can make your money grow over time, but emergencies happen. Getting this wrong could leave you scrambling when life hits hard or missing out on years of potential gains.

This guide is for anyone wondering whether an emergency fund vs investing should be their first financial priority – from recent graduates with their first paycheck to career changers building financial stability from scratch.

We’ll walk through why building your financial safety net comes first and how it actually protects your future investments. You’ll learn investment fundamentals that work once you have that security blanket in place. Then we’ll show you how to create a strategic balance between emergency savings and investment so you’re not stuck choosing one or the other forever.

Money decisions don’t have to be this complicated. Let’s figure out the right order for your situation.

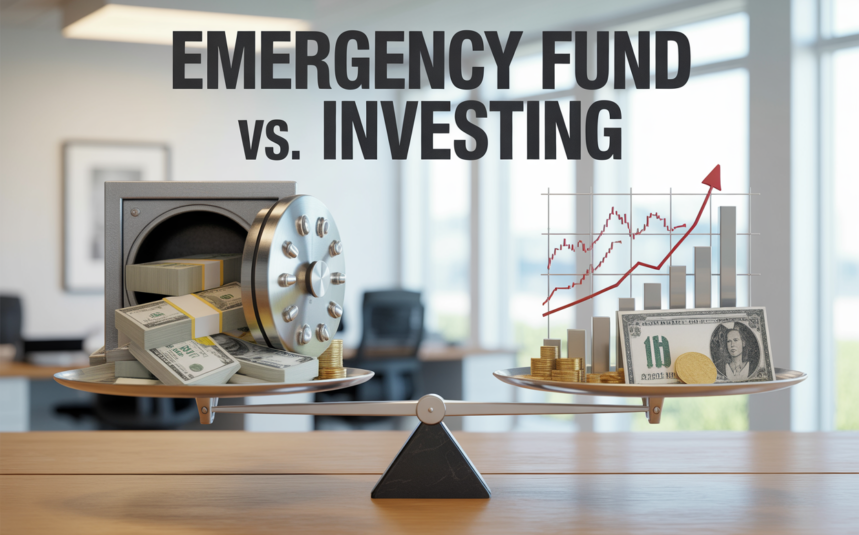

Build Your Financial Safety Net First

Why Emergency Funds Protect Your Long-Term Goals

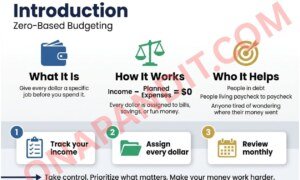

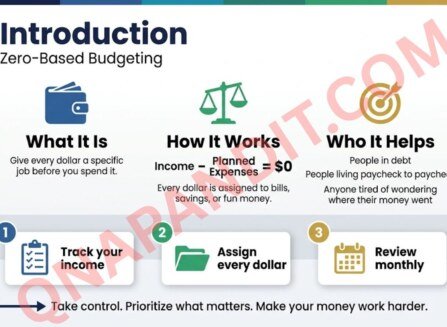

An emergency fund serves as your financial safety cushion for unexpected expenses, helping you avoid debt or selling important assets during surprises like car breakdowns, unexpected bills, or illness. This safety net provides security and reduces worry about unexpected costs, protecting you from sudden expenses like home repairs or medical emergencies without altering your normal spending habits. Most importantly, an emergency fund safeguards your financial stability by preventing short-term crises from derailing long-term financial goals. Investing without an emergency fund can force you to sell investments prematurely, potentially at a loss if the market is down, disrupting the powerful effects of long-term compounding that build true wealth.

Calculate Your Ideal Emergency Fund Size

A good rule of thumb is to save three to six months of living costs, though financial planners often recommend six to nine months of essential living expenses. The ideal fund size depends on several personal factors,s including job stability, the number of income earners in your household, monthly expenses, and your comfort level with risk. When calculating your target amount, focus on essential expenses, es including rent or home loan payments, groceries, utilities, insurance premiums, and transportation costs. Individuals in volatile jobs, freelancers, entrepreneurs, or those in senior roles requiring longer to replace may need a larger emergency reserve to maintain financial security.

Choose the Right Account for Quick Access

Your emergency fund must be easily accessible, ideally kept in a high-interest savings account or other highly liquid instruments. Financial planners suggest keeping emergency savings in accounts that allow quick withdrawals while offering modest returns, prioritising capital safety over higher yields. Keeping emergency funds in volatile investments like equities is generally not recommended, as market fluctuations could reduce their value precisely when you need the money most, and withdrawals may take longer during critical situations when immediate access is essential.

Avoid Common Emergency Fund Mistakes

The most critical mistake is investing your emergency fund, as its primary purpose is quick access and capital safety, not growth. Never stop building your emergency fund, even when you start investing, as both serve different but equally important roles in your financial strategy. Ensure your emergency fund is adequately sized for your personal situation rather than following generic advice that may not match your specific circumstances and risk profile.

Master Investment Fundamentals for Wealth Growth

Understand Different Investment Types and Their Risks

Investing means allocating money to assets like stocks, bonds, mutual funds, and ETFs to grow wealth over time for long-term aspirations such as retirement or homeownership. While offering significant growth potential compared to savings accounts, investing always carries risks. Stocks represent company ownership with fluctuating values based on performance, offering potential gains but also losses. Bonds involve lending money to governments or companies, providing returns with typically lower risk and returns than stocks. Mutual funds pool investor money to buy diversified portfolios managed by professionals, spreading risk but including management fees. ETFs function similarly but trade on exchanges like individual stocks.

Harness the Power of Starting Early and Compounding

Starting investments early proves crucial due to compounding interest, where earnings are reinvested to generate additional earnings, leading to substantial wealth growth over time. Early investment fundamentals provide more time to ride out market fluctuations—despite short-term volatility, investments tend to trend upwards over the long term, allowing recovery from lows and greater gains. This extended timeline becomes your greatest advantage in building wealth.

Balance Risk Based on Your Timeline and Goals

Your investment strategy should align with your risk comfort level and timeline. Those nervous about losses might prioritise emergency savings vs investment initially. Short-term financial goals suit savings accounts better, while long-term goals benefit from investment growth. Money needed soon should remain accessible in savings, whereas funds for distant goals can be invested to maximise growth potential through a strategic wealth-building strategy.

Create a Strategic Balance Between Safety and Growth

Assess Your Current Financial Situation and Stability

Begin by evaluating your income stability, as irregular earnings may necessitate a larger emergency fund. Review existing debt, especially high-interest obligations like credit card debt, as it can impede both saving and investing efforts. Determine if you have an existing nest egg, which might indicate readiness to increase investment contributions.

Build Emergency Savings While Starting Small Investments

Financial planning doesn’t require an either/or choice between an emergency fund and investing. Many individuals find success by gradually building their emergency fund while simultaneously starting small, systematic investments through mutual fund SIPs. This balanced approach fosters both financial security and wealth-building habits simultaneously. Once your initial emergency fund goal is met, you can prioritise investing more money while continuing to maintain your emergency savings.

Adjust Your Strategy Based on Income Stability and Life Stage

Your strategy for emergency fund size should adapt to factors like job stability, the number of income earners in your household, and overall monthly expenses. Individuals in stable jobs might find six months of expenses sufficient, while those in volatile sectors, freelancers, or entrepreneurs may benefit from a larger reserve. Major life events, such as marriage, starting a family, or planning for retirement, significantly impact your financial needs and necessitate adjustments to your savings and investment strategy.

Overcome Common Financial Planning Obstacles

Manage Tight Budgets with Smart Spending Cuts

When facing a tight budget, meticulously review your spending to distinguish between essential needs and discretionary expenses. Focus on cutting back on unnecessary spending and seeking cheaper alternatives for other expenses to free up more money for savings or investments.

Generate Additional Income to Boost Both Savings and Investments

Explore opportunities to generate additional income through part-time work, freelance gigs, or by monetising a hobby. Extra income can significantly boost both your savings and investment funds, accelerating financial progress toward building your emergency fund while simultaneously growing wealth through strategic investments.

Break Through Mental Barriers That Prevent Financial Progress

Overcome the fear of losing money in investments by educating yourself on investment principles and starting with safer, lower-risk options. Recognise that investing is typically a long-term endeavour where patience often yields rewards. Dispel the misconception that a large sum of money is required to start investing; many accessible options allow individuals to begin with small amounts.

Leverage Tools and Expert Guidance for Success

Use Technology to Track Spending and Automate Savings

Now that we’ve covered the fundamental strategies, leveraging technology can significantly streamline your financial planning process. Financial planning apps like YNAB (You Need A Budget) and PocketGuard effectively monitor spending patterns and identify savings opportunities within your budget. Spending tracker apps such as Expensify and Wally prove particularly valuable for self-employed individuals and small business owners managing complex expense categories. Many financial institutions now offer integrated tools like Neo Insights, which simplifies spending tracking by providing instant breakdowns by time, category, and transaction while using AI to analyse your financial habits and patterns.

Recognise When Professional Financial Advice Is Worth the Investment

Professional financial guidance becomes essential when navigating complex situations involving business ownership, managing family financial issues, or paying off substantial debt loads. Consider consulting a financial advisor when planning serious investment moves or managing significant sums of money that require sophisticated wealth-building strategies. Major life events like marriage, having a baby, or planning for retirement significantly alter your financial needs and priorities, making professional input invaluable. Financial advisory services excel at designing personalised financial plans that effectively balance security, growth, and long-term wealth creation while addressing your specific emergency fund vs investing priorities.

Building your financial future requires both protection and growth, and the choice between an emergency fund and investing isn’t truly an either-or decision. The most effective approach starts with establishing your financial safety net—saving three to six months of essential expenses in an easily accessible account—before pursuing aggressive investment strategies. This foundation ensures that unexpected expenses won’t force you to liquidate investments at unfavourable times, protecting both your immediate stability and long-term wealth-building goals.

Once your emergency fund reaches an adequate level, you can confidently shift focus toward investing for growth while maintaining that crucial financial buffer. Remember that you don’t need large amounts to begin investing, and many tools and resources are available to help you manage both savings and investments effectively. Start small, build consistently, and consider seeking professional guidance when facing complex financial decisions or major life changes. The key is taking that first step today—whether it’s opening a high-yield savings account for emergencies or beginning your investment journey with whatever amount you can comfortably set aside.