How to Start a Blog Without These 5 Costly Beginner Errors

Starting a blog feels like launching into uncharted territory. You’re ready to share your expertise with the world, but one wrong move can waste months of effort and hundreds of dollars. This guide is for aspiring bloggers and business owners who want to build a successful blog from day one. We’ll walk through how to […]

Can I save money without cutting my lifestyle drastically?

Yes, it is possible to save money without drastically cutting your lifestyle by implementing some smart strategies and making conscious decisions. Here's how you can do it: 1. Budgeting: Create a detailed budget to track your income and expenses. Identify areas where you can cut back without signifiRead more

Yes, it is possible to save money without drastically cutting your lifestyle by implementing some smart strategies and making conscious decisions. Here’s how you can do it:

1. Budgeting: Create a detailed budget to track your income and expenses. Identify areas where you can cut back without significantly impacting your lifestyle.

2. Reduce Unnecessary Expenses: Review your spending habits and identify items or services you can live without. Cut back on dining out, subscription services, or impulse purchases.

3. Prioritize Savings: Treat savings like a recurring expense. Set up automated transfers to your savings account each month before you spend on non-essentials.

4. Comparison Shopping: Compare prices before making significant purchases. Look for discounts, coupons, and deals to save money without sacrificing quality.

5. Meal Planning: Plan your meals ahead to avoid wastage and unnecessary trips to the grocery store. Cook at home more often to save on dining expenses.

6. Seek Discounts and Rewards: Take advantage of loyalty programs, cashback rewards, and discounts offered by retailers to save money on everyday purchases.

7. Review Subscriptions: Identify and cancel any unused or unnecessary subscriptions like gym memberships, streaming services, or magazine subscriptions.

8. Energy Efficiency: Save on utility bills by being mindful of energy consumption. Turn off lights and unplug devices when not in use, and consider energy-efficient appliances.

By implementing these practical tips, you can start saving money without drastically altering your lifestyle. Remember,

See lessHow many goldbees is 1 gram of gold?

One gram of gold is approximately equivalent to 62.2 "goldbees."- "Goldbee" is a fictional term not recognized in the standard units of measurement.- The question seems to be a play on words or a made-up concept rather than based on factual information.- Gold weight is typically measured in grams, oRead more

One gram of gold is approximately equivalent to 62.2 “goldbees.”

– “Goldbee” is a fictional term not recognized in the standard units of measurement.

– The question seems to be a play on words or a made-up concept rather than based on factual information.

– Gold weight is typically measured in grams, ounces, or troy ounces, not in unconventional units like “goldbees.”

– To determine the amount of gold in grams, you can use a precise weighing scale designed for small weights.

Hope this helps—feel free to add your experience or ask a follow-up.

See lessHow do I create an emergency fund from scratch?

Creating an emergency fund from scratch is a crucial step in achieving financial stability and peace of mind. Here's a detailed guide on how to build an emergency fund effectively:Step 1: Set a Clear Goal- Determine how much you want to save for your emergency fund. A common recommendation is to havRead more

Creating an emergency fund from scratch is a crucial step in achieving financial stability and peace of mind. Here’s a detailed guide on how to build an emergency fund effectively:

Step 1: Set a Clear Goal

– Determine how much you want to save for your emergency fund. A common recommendation is to have 3 to 6 months’ worth of living expenses.

Step 2: Track Your Expenses

– Analyze your monthly expenses to understand your spending habits and identify areas where you can cut back to save more.

Step 3: Create a Budget

– Develop a realistic budget that allocates a portion of your income towards your emergency fund. Consider using budgeting tools or apps to help you stay on track.

Step 4: Start Small and Be Consistent

– Begin by setting achievable savings goals. Even saving a small amount regularly can add up over time. Consistency is key.

Step 5: Choose the Right Savings Account

– Opt for a high-yield savings account or a money market account that offers competitive interest rates to help your money grow faster.

Step 6: Automate Your Savings

– Set up automatic transfers from your checking account to your emergency fund to ensure a consistent savings habit.

Step 7: Reassess and Adjust

– Periodically review your budget and savings goals. Adjust as needed based on changes in your income or expenses.

Common Mistakes to Avoid:

– Not Prioritizing Emergency Fund:

See lessIs the 50/30/20 budgeting rule effective?

The 50/30/20 budgeting rule, popularized by Senator Elizabeth Warren in her book "All Your Worth: The Ultimate Lifetime Money Plan," is a simple and effective guideline for managing personal finances. Here's an overview of the rule's effectiveness and some key points to consider:What is the 50/30/20Read more

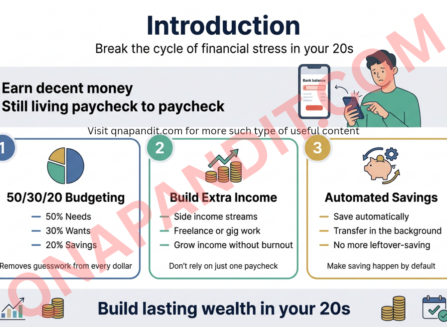

The 50/30/20 budgeting rule, popularized by Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan,” is a simple and effective guideline for managing personal finances. Here’s an overview of the rule’s effectiveness and some key points to consider:

What is the 50/30/20 Budgeting Rule?

1. 50% Needs, 30% Wants, 20% Savings/Debt Repayment:

– Allocate 50% of your after-tax income to necessities like housing, utilities, food.

– Dedicate 30% to discretionary expenses such as dining out, shopping, entertainment.

– Save 20% for financial goals like emergency fund, retirement savings, debt payments.

Effectiveness of the Rule:

1. Simplicity and Clarity:

– Easy-to-understand framework for budgeting.

– Provides a balanced approach to managing finances.

2. Promotes Financial Health:

– Encourages saving and debt reduction.

– Helps prioritize spending on essentials over wants.

3. Personalization:

– Can be adjusted based on individual circumstances.

– Serves as a foundation for building a more detailed budget.

Hidden Pain Points and Considerations:

1. Variability:

– Fixed living costs may exceed 50%, especially in high-cost areas.

– Personal situations might require flexibility in the allocation percentages.

2. **Emergency Fund

See lessHow much of my income should I save each month?

When it comes to saving a portion of your income each month, it's essential to strike a balance between meeting your current financial needs and securing your future financial stability. While the exact percentage may vary based on individual circumstances, financial experts generally recommend follRead more

When it comes to saving a portion of your income each month, it’s essential to strike a balance between meeting your current financial needs and securing your future financial stability. While the exact percentage may vary based on individual circumstances, financial experts generally recommend following the 50/30/20 rule for personal finance:

– 50% for Needs: Allocate approximately 50% of your income towards essential expenses like housing, utilities, groceries, transportation, and insurance.

– 30% for Wants: Reserve around 30% for discretionary spending on non-essential items such as dining out, entertainment, hobbies, and shopping.

– 20% for Savings: Aim to save at least 20% of your income each month. This portion can go towards various savings goals, including emergency fund, retirement savings, investments, and other financial objectives.

By prioritizing savings and making it a non-negotiable part of your budget, you establish a healthy financial habit that can lead to long-term wealth accumulation and financial security.

Remember, the key to successful saving is consistency and discipline. Automating your savings through direct deposit or setting up recurring transfers to a separate savings account can help you stay on track without the temptation to spend the money elsewhere.

Additionally, consider optimizing your savings by:

– Regularly reviewing and adjusting your budget to ensure your savings rate aligns with your financial goals.

– Maximizing contributions to tax-advantaged accounts like 401(k)s, IRAs, or other retirement savings

See lessWhat are the best apps to track monthly expenses?

Tracking monthly expenses is crucial for financial management. Here are some of the best apps that can help you effectively track your expenses: 1. Mint: A popular and comprehensive app that allows you to connect your accounts to track expenses, create budgets, and set financial goals. Mint also proRead more

Tracking monthly expenses is crucial for financial management. Here are some of the best apps that can help you effectively track your expenses:

1. Mint: A popular and comprehensive app that allows you to connect your accounts to track expenses, create budgets, and set financial goals. Mint also provides insights into your spending habits and helps you stay on top of your finances.

2. You Need a Budget (YNAB): YNAB is a budgeting app that focuses on giving every dollar a job. It encourages you to assign your income to specific categories, track your expenses, and make informed financial decisions.

3. PocketGuard: This app gives you a snapshot of your financial situation by tracking your income, bills, and spending in one place. It also helps identify areas where you can cut back expenses and save money.

4. GoodBudget: GoodBudget uses the envelope system to allocate your money to different spending categories. It allows you to track your expenses manually, making you more aware of where your money is going.

5. Personal Capital: While known for its investment tracking features, Personal Capital also offers tools to track your expenses, manage your budget, and plan for your financial future.

Key Points:

– These apps offer a range of features to suit different financial management styles, from automated tracking to manual input.

– They provide insights into your spending habits, help you set financial goals, and ultimately empower you to make more informed financial decisions.

– Each app has

See lessHow can I start saving money on a tight budget?

Starting to save money on a tight budget requires discipline and strategic planning. Here are some effective tips to help you begin your savings journey even with limited financial resources: 1. Create a Budget: Establish a detailed budget outlining your income and expenses. This will help you identRead more

Starting to save money on a tight budget requires discipline and strategic planning. Here are some effective tips to help you begin your savings journey even with limited financial resources:

1. Create a Budget: Establish a detailed budget outlining your income and expenses. This will help you identify areas where you can reduce spending and allocate more towards saving.

2. Track Your Expenses: Keep track of every penny you spend to pinpoint areas where you can cut back. Utilize budgeting apps or spreadsheets to make this process easier.

3. Reduce Unnecessary Spending: Identify non-essential expenses that can be eliminated or minimized. This could include eating out less, cutting down on subscription services, or finding more affordable alternatives for your regular expenses.

4. Automate Your Savings: Set up automatic transfers from your checking account to your savings account. Even small, regular amounts can add up over time and make a significant difference.

5. Opt for Generic Brands: Consider opting for generic brands instead of name brands for groceries and other items. You can often get similar quality at a lower price.

6. Shop Smart: Look for sales, discounts, and coupons when making purchases. Buying in bulk for frequently used items can also lead to cost savings in the long run.

7. Cook at Home: Eating out can quickly deplete your budget. Plan your meals, cook at home, and pack your lunch for work to save a significant amount of money.

8. Negotiate Bills: Call

See lessWhat is el nino ?

El Niño is a climatic phenomenon that occurs in the Pacific Ocean, characterized by the warming of sea surface temperatures. Here's a comprehensive explanation to address various aspects:What is El Niño?- El Niño refers to the irregular warming of sea surface temperatures in the central and easternRead more

El Niño is a climatic phenomenon that occurs in the Pacific Ocean, characterized by the warming of sea surface temperatures. Here’s a comprehensive explanation to address various aspects:

What is El Niño?

– El Niño refers to the irregular warming of sea surface temperatures in the central and eastern tropical Pacific Ocean.

– This phenomenon is part of the broader El Niño-Southern Oscillation (ENSO) cycle that includes El Niño, La Niña, and neutral phases.

– El Niño events typically last about 9-12 months but can persist for up to two years.

– One of the key indicators of El Niño is the weakening of trade winds in the Pacific, leading to a cascade of global climate impacts.

Common Confusions and Misconceptions:

– Misconception: El Niño only affects weather patterns in the Pacific region.

– Clarification: El Niño influences weather patterns globally, leading to droughts, floods, and other extreme weather events in various parts of the world.

– Misconception: El Niño and climate change are the same.

– Clarification: While climate change can influence the frequency and intensity of El Niño events, they are distinct phenomena with different underlying causes.

Impacts of El Niño:

– El Niño can lead to:

– Droughts in some regions (e.g., Australia, Indonesia).

– Heavy rainfall and floods in others (e.g., South

See lessCan I launch my own crypto token?

Yes, you can launch your own crypto token. Here's a comprehensive guide on how to go about it: 1. Understand the Type of Token: Determine whether you want to create a utility token, security token, or a stablecoin. Each type has specific use cases and regulatory considerations. 2. Choose the BlockchRead more

Yes, you can launch your own crypto token. Here’s a comprehensive guide on how to go about it:

1. Understand the Type of Token: Determine whether you want to create a utility token, security token, or a stablecoin. Each type has specific use cases and regulatory considerations.

2. Choose the Blockchain Platform: Select a blockchain platform to build your token on. Ethereum is commonly used for creating tokens due to its smart contract functionality, but other platforms like Binance Smart Chain and Solana are also popular.

3. Create a Whitepaper: Develop a detailed whitepaper that outlines the purpose of your token, its utility, distribution, tokenomics, and the problem it aims to solve.

4. Smart Contract Development: Write a smart contract for your token that defines its functionalities, such as token creation, distribution, transfers, and possible burning mechanisms.

5. Token Distribution: Decide on the token distribution model. Will tokens be sold through an initial coin offering (ICO), airdropped, or distributed through other means?

6. Legal Compliance: Ensure that you comply with relevant regulations in the jurisdictions you operate in. Consult legal experts to understand the regulatory requirements for launching a crypto token.

7. Marketing and Community Building: Develop a solid marketing strategy to create awareness about your token. Engage with the community through social media, forums, and other channels to build interest.

8. Launch and Maintenance: Once everything is in place, launch your token

See lessIs It Cheaper to Fly or Take a Train from Boston to New York?

When deciding whether to fly or take a train from Boston to New York, several factors come into play that can help you determine which option is cheaper and more convenient. Here's a detailed comparison to help you make an informed decision:Flight from Boston to New York:- Cost:- The cost of a flighRead more

When deciding whether to fly or take a train from Boston to New York, several factors come into play that can help you determine which option is cheaper and more convenient. Here’s a detailed comparison to help you make an informed decision:

Flight from Boston to New York:

– Cost:

– The cost of a flight can vary greatly depending on the airline, time of booking, and day of travel. Last-minute flights are usually more expensive.

– Additional fees for luggage, seat selection, and onboard services can drive up the total cost.

– Duration:

– The flight itself is short, typically around 1 hour, but when factoring in travel time to the airport, security checks, boarding, and potential delays, the total travel time can be longer.

– Convenience:

– Airports in both Boston and New York are usually located outside the city center, requiring additional time and cost for ground transportation.

Train from Boston to New York:

– Cost:

– Train tickets are generally more consistent in price and may offer discounts for booking in advance or for specific times.

– There are usually no additional fees for luggage or seat selection.

– Duration:

– The train ride itself takes around 3-4 hours, but train stations are typically located in or near city centers, saving time on ground transportation.

– Trains are less prone to delays compared to flights.

– Convenience:

– Tr

See less