What credit score is needed for VA loan?

Latest News & Updates

QNAPANDIT Latest Articles

Don’t Use ChatGPT Until You Try This Money Trick

Most entrepreneurs chase ChatGPT money-making tricks but end up with nothing to show for their efforts. This guide is for business owners and side hustlers who want to actually profit from AI instead of just collecting screenshots and hoping for the best. ChatGPT won’t magically print money. The real opportunity lies in using AI business […]

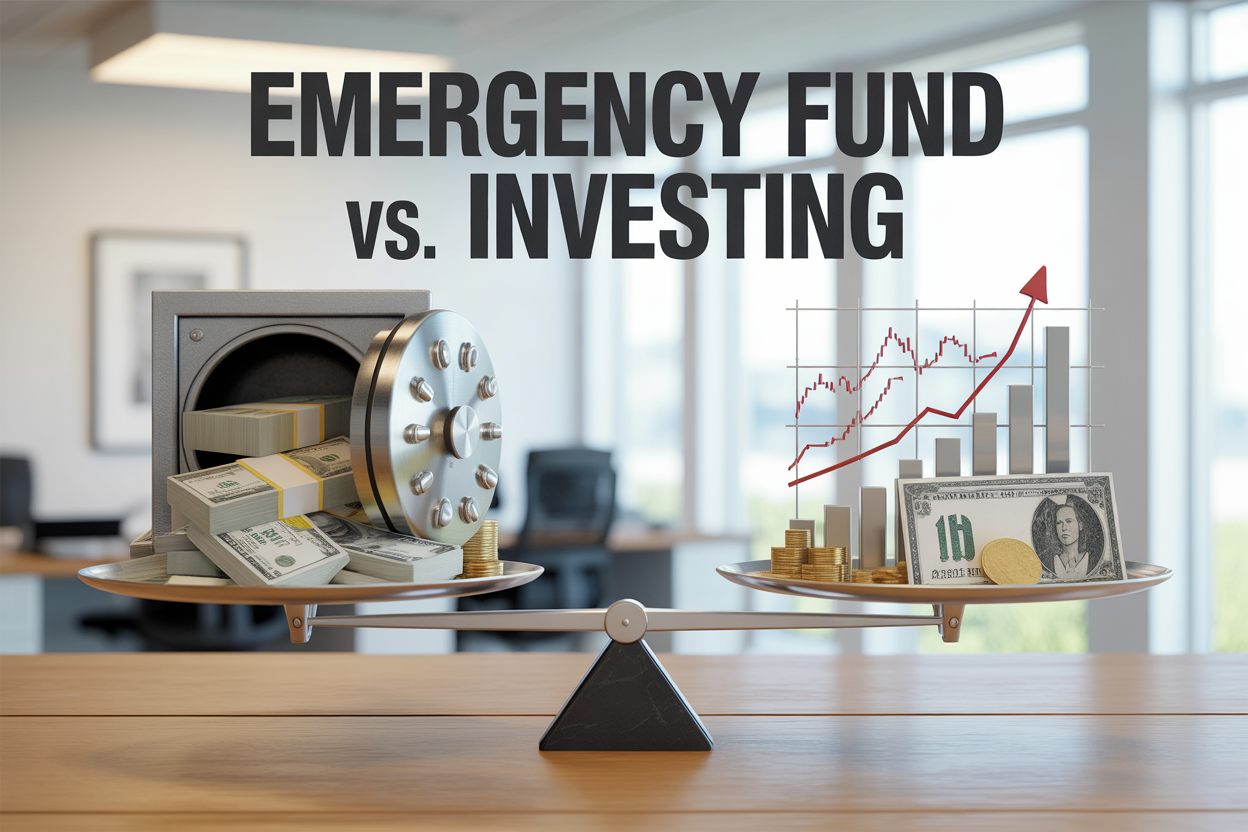

Emergency Fund vs. Investing: Which Should Come First?

You’ve got money to manage, but you’re stuck on a big question: Should you build an emergency fund or start investing first? This decision stumps many people, especially young adults and new earners who want to grow wealth but also need financial security. You know investing can make your money grow over time, but emergencies […]

Why Most Bloggers Ignore PAA (And Miss 40% More Traffic)

Most bloggers are leaving serious money on the table by ignoring one of Google’s most visible features. If you’re a content creator, digital marketer, or business owner struggling to increase organic traffic despite publishing consistently, you’re not alone. Over 80% of blogs fail within 18 months, and one major reason is overlooking People Also Ask […]

This ONE Legal Trick Boosted My Credit Score 200 Points in 30 Days!

Your credit score is tanking and you need results fast. Maybe you’re trying to qualify for a mortgage, get approved for that car loan, or finally move into your dream apartment. Whatever your reason, you’re not alone – millions of Americans struggle with low credit scores that block them from financial opportunities. This guide is […]

How to attract and retain top Salesforce developer talent

The Salesforce talent market is red-hot, and finding skilled developers is just half the battle. The real challenge? Keeping them on your team once you’ve hired them. This guide is for hiring managers, HR leaders, and team leads who want to build and maintain high-performing Salesforce development teams. With developer demand far outpacing supply, your […]

How to Choose a Domain When Your Perfect Name Is Taken

How to Choose a Domain When Your Perfect Name Is Taken Finding out your dream domain name taken can feel like a punch to the gut. You’ve brainstormed the perfect name for your business or blog, only to discover someone else got there first. This guide is for entrepreneurs, bloggers, and anyone launching a website […]

Why PAA Questions Are SEO Gold (And How to Mine Them)

Google’s People Also Ask boxes appear in over 43% of search results, yet most marketers ignore this goldmine of SEO opportunities. PAA questions reveal exactly what your audience wants to know, giving you a direct path to featured snippets, voice search optimization, and higher rankings. This guide is for content marketers, SEO specialists, and business […]

The Shocking Truth About Home Yoga That Studios Don’t Want You to Know

Studios charge premium prices for what we can achieve right in our living rooms – and the home yoga benefits often surpass traditional classes. This guide is for busy people who want to start yoga at home, for beginners, experienced practitioners seeking flexibility, and anyone tired of expensive studio memberships that don’t fit their schedule. […]

2026 Budget Planner for Beginners: Zero-Based Budgeting Guide

Ready to take control of your money in 2026? Zero-based budgeting might be exactly what you need to finally see where every dollar goes. This 2026 budget planner for beginners will show you how zero-based budgeting works – a simple method where your income minus expenses equals zero every month. Don’t worry, that doesn’t mean […]

10 Online Business Ideas Under ₹50,000 (India, 2026 Edition)

Starting an online business in India doesn’t need to break your bank account. With just ₹50,000, you can launch a profitable venture from your home and tap into India’s booming digital economy. This guide is perfect for college students, working professionals seeking side income, and aspiring entrepreneurs who want to start small and scale smartly. […]

5 Morning Habits That Boost Energy Without Coffee

Tired of depending on coffee to jumpstart your day? You’re not alone. Many people struggle with low energy in the morning and wonder how to wake up energised without coffee. The good news is that simple, natural morning habits can boost energy levels just as effectively as your daily cup of joe. This guide is […]

The Ultimate SEO Toolkit: 5 Must-Have Tools for 2026

SEO success in 2026 demands more than traditional keyword stuffing and link building. You need tools that can navigate AI-powered search engines, track your brand’s visibility in ChatGPT responses, and optimise for Google’s AI Overviews alongside classic organic rankings. This guide is designed for digital marketers, content creators, SEO professionals, and business owners who want […]

7 Tech Trends That Will Transform Your Life by 2030

Technology is advancing faster than ever, and by 2030, several breakthrough innovations will completely change how you live, work, and interact with the world around you. This guide is for tech enthusiasts, business professionals, and anyone curious about the future who wants to understand which emerging technologies will have the biggest impact on daily life. […]

Why Closing Old Credit Cards Could Destroy Your Score

Closing old credit cards can tank your credit score in ways most people don’t expect. This guide is for anyone considering cancelling old cards, whether you’re decluttering your wallet or avoiding annual fees. Your credit score takes a hit primarily because closing credit cards affects your credit utilisation ratio. When you lose that available credit […]

How to Rebuild Your CIBIL Score After Settlement in 6 Months

Settled a loan and watching your CIBIL score plummet? You’re not alone. Thousands of borrowers face the same challenge after choosing settlement over prolonged EMI struggles, but the good news is that CIBIL score improvement after settlement is absolutely possible with the right approach. This guide is for anyone who has recently settled a loan […]

Understanding Your Audience: The Foundation of Resonance

Why Audience Understanding is Non-Negotiable Creating content without understanding your audience is like shooting arrows in the dark – you might occasionally hit something, but most efforts miss their mark entirely. Audience understanding forms the bedrock of effective content strategy, transforming generic information into powerful messaging that resonates. When you deeply understand your audience, you […]

Best Side Hustles to Make Money Online in 2026

The internet has completely transformed the way people earn money. What started as freelancing and blogging years ago has evolved into a massive digital economy filled with opportunities for creators, freelancers, entrepreneurs, students, remote workers, and even complete beginners. In 2026, side hustles are no longer just “extra income” ideas. For many people, they’ve become […]

Transforming the Educational Landscape: The Value of an Education Franchise in Nigeria

The global demand for high-quality supplementary learning has witnessed a dramatic surge over recent years. In rapidly developing economies, traditional academic structures face massive challenges trying to keep pace with the cognitive and technological skills required for the modern global workforce. As a result, parents are increasingly looking for specialized programs that go beyond basic […]

How to Turn Your Hobby Into a Profitable Career Skill

Your hobby feels more like an escape from work than just a weekend activity. We get it—that creative spark or hands-on satisfaction you find in photography, cooking, woodworking, or whatever gets you excited might actually be pointing toward your next career move. This guide is for anyone tired of watching the clock at their day […]

Crypto Portfolio Strategy 2026: Safe Diversification in INR

Building a smart crypto portfolio in 2026 means more than just buying Bitcoin and hoping for the best. With institutional money pouring into crypto ETFs and new asset classes like tokenised real estate hitting the scene, Indian investors need a structured approach to spread risk across this volatile market while keeping their rupee investments safe. […]

Timur Turlov and the Global Development of Freedom Holding

In recent years, financial entrepreneur Timur Turlov has attracted attention in the global finance sector as the founder and CEO of Freedom Holding Corp. As financial markets become more interconnected and technology reshapes how investors access global exchanges, companies like Freedom Holding represent a broader shift toward modern, digital-driven financial services. Freedom Holding Corp. operates […]

How to Write a Business Plan (India, 2026): Step-by-Step

Starting a business in India has never been more accessible, but turning your idea into reality still requires a solid plan. This comprehensive guide shows you how to write a business plan that actually works for Indian entrepreneurs in 2026. This step-by-step business plan guide is designed for first-time entrepreneurs, startup founders, and small business […]

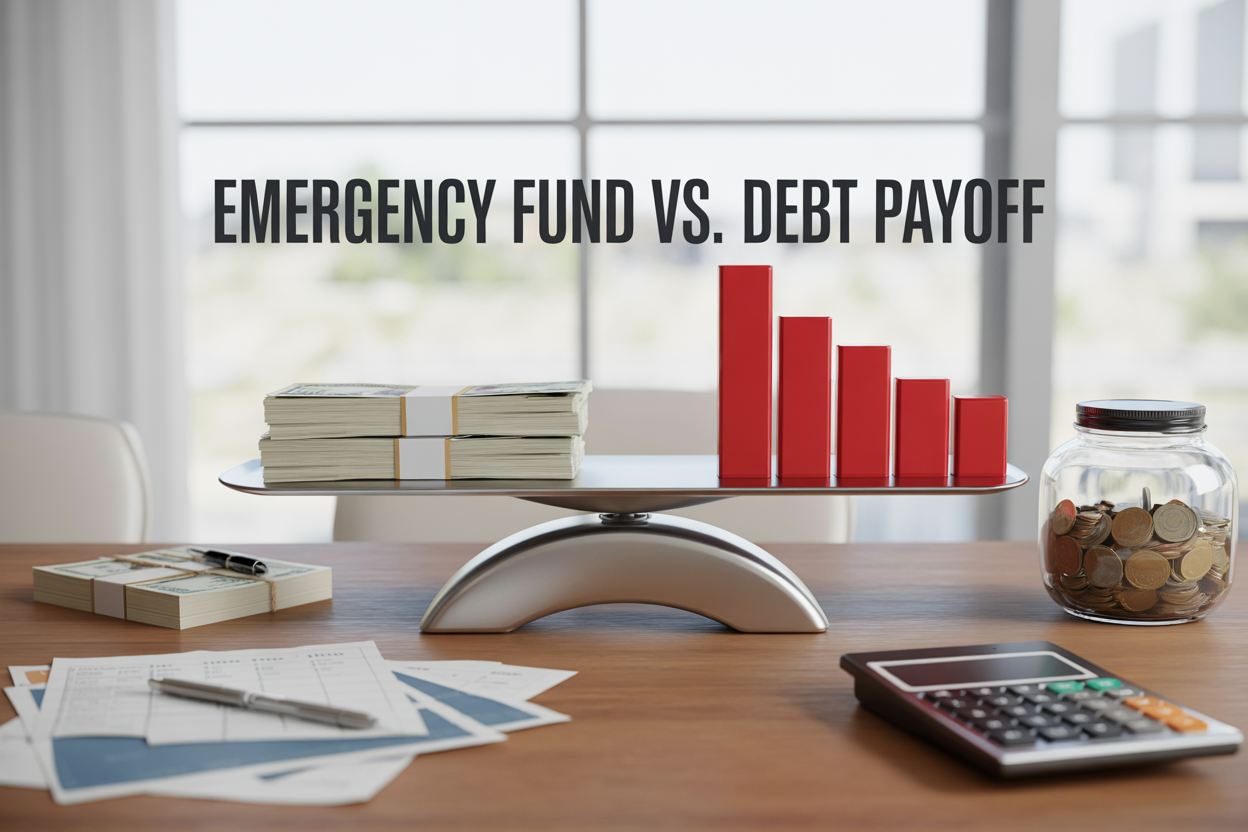

Emergency Fund vs. Debt Payoff: Which Should Come First?

You’re staring at credit card bills and an empty savings account, wondering where to put your next paycheck. The emergency fund vs debt payoff dilemma affects millions of Americans who feel stuck between building financial security and eliminating high-interest debt. This guide is for anyone juggling debt payments while trying to save money—whether you’re recovering […]

The Ultimate Guide to Avoiding Package Delivery Scams

Package delivery scams are exploding as more Americans shop online and expect regular deliveries. These scams target anyone waiting for packages, using fake delivery notifications and phishing delivery emails to steal your money and personal information. You’re especially vulnerable if you frequently order online, live in an apartment complex, or recently made purchases from unfamiliar […]

Freelancer’s Guide to Starting a One-Person Business (2026 Blueprint)

Ready to ditch the 9-to-5 and build something that’s truly yours? This freelancer’s guide to starting a one-person business shows you exactly how to transform your skills into a profitable solo venture in 2026. This blueprint is designed for ambitious freelancers, side hustlers looking to go full-time, and anyone who wants to escape the traditional […]

The Ultimate Guide to Boosting Your Credit Score in 90 Days

A poor credit score can cost you thousands of dollars in higher interest rates and limit your access to loans, apartments, and even some jobs. If you’re dealing with bad credit from past mistakes, preparing for a major purchase, or simply want to improve your financial standing, this 90-day credit improvement plan can help you […]

Erotica AI: Advancing Adult Fiction in the Digital Age

Artificial intelligence is steadily transforming creative industries, and one of its more specialised directions is erotica AI. Built on sophisticated language models, this technology can generate romantic and adult-themed stories from simple prompts. Instead of replacing authors, erotica AI serves as a creative assistant, helping users shape ideas, organise plots, and develop compelling characters with […]

How to Start Crypto Staking in India: Earn Passive Crypto Income

Crypto staking lets you earn passive income from your digital assets while supporting blockchain networks. If you’re an Indian crypto investor looking to generate steady returns without active trading, staking offers a compelling opportunity to put your cryptocurrency to work. This guide is designed for beginners who want to start earning crypto staking rewards in […]

If you are a Veteran or an active-duty service member looking to buy a home, I have some great news for you. Technically, the Department of Veterans Affairs (VA) does not have a set minimum credit score requirement. This makes the VA home loan one of the most flexible options out there! However, whiRead more

If you are a Veteran or an active-duty service member looking to buy a home, I have some great news for you. Technically, the Department of Veterans Affairs (VA) does not have a set minimum credit score requirement. This makes the VA home loan one of the most flexible options out there!

See lessHowever, while the government doesn’t set a number, the private banks and mortgage companies that actually give you the money usually do. In 2026, most lenders are looking for a FICO score of at least 620. Think of the VA as a co-signer that makes the bank feel safe, but the bank still wants to know you have a history of paying your bills on time.

If your score is a bit lower, like 580, don’t give up! Some specialized lenders work specifically with lower scores. The key is to show that you have a steady income and not too much other debt. It’s always a good idea to check your credit report early so you can fix any small mistakes before you start house hunting.

The question of credit requirements for the VA Home Loan program is often misunderstood due to the "dual-gate" nature of the approval process. As a professional in the mortgage industry for decades, I can tell you that navigating this requires understanding the distinction between VA Agency GuidelinRead more

The question of credit requirements for the VA Home Loan program is often misunderstood due to the “dual-gate” nature of the approval process. As a professional in the mortgage industry for decades, I can tell you that navigating this requires understanding the distinction between VA Agency Guidelines and Lender Overlays.

The Absence of a Federal Minimum

According to the VA Lenders Handbook (Pamphlet 26-7), the Department of Veterans Affairs does not establish a minimum FICO score. Instead, the VA requires that a borrower be a “satisfactory credit risk.” This ambiguity is intentional, allowing for a holistic review of a Veteran’s financial profile. However, in the secondary market where these loans are packaged into GNMA (Ginnie Mae) securities, risk appetite dictates the practical floor.

Understanding Lender Overlays and the 2026 Climate

While the VA is silent on the number, private lenders almost universally implement overlays. As of early 2026, the industry standard for an “Approve/Eligible” finding via Automated Underwriting Systems (AUS) typically begins at a 620 median FICO. However, we are seeing a trend where “non-bank” lenders are pushing deep into the 550–580 range to capture volume in a competitive rate environment.

The Role of Residual Income

The “secret sauce” of VA lending isn’t actually the credit score—it’s Residual Income. Unlike conventional loans that rely heavily on Debt-to-Income (DTI) ratios, the VA uses a formula to ensure you have a specific dollar amount left over each month for family support (food, gas, etc.) based on your region and family size. A borrower with a 580 score but substantial residual income and a clean 12-month housing payment history is often a stronger candidate than a 660-score borrower with no cash reserves.

Manual Underwriting Nuances

For those below the 620 threshold, manual underwriting becomes the path forward. In this scenario, underwriters scrutinise:

In summary, while 620 is the safe bet, the program’s primary focus is on your ability to pay and residual cash flow. Always ensure your Certificate of Eligibility (COE) is in hand before engaging in high-level underwriting discussions.

See lessLooking for the "short version"? Here is the breakdown for VA loan credit scores in 2026: VA Government Requirement: None. The VA does not set a minimum score. Typical Lender Requirement: 620 is the industry standard for most banks. Flexible Lenders: Some specialised VA lenders will accept scores asRead more

Looking for the “short version”? Here is the breakdown for VA loan credit scores in 2026:

-

VA Government Requirement: None. The VA does not set a minimum score.

-

Typical Lender Requirement: 620 is the industry standard for most banks.

-

Flexible Lenders: Some specialised VA lenders will accept scores as low as 550 to 580.

-

Best Rates: To get the most competitive interest rates in 2026, aim for a score of 720 or higher.

-

Beyond the Score: Lenders care more about your residual income (cash left after bills) and your last 12 months of on-time rent/mortgage payments than just the 3-digit number.

-

Manual Underwriting: If your score is below 620, expect a human underwriter to do a more detailed review of your finances.

See lessThe VA does not have a minimum credit score requirement, but most private lenders require a minimum FICO score of 620. Some specialized lenders may approve VA loans with scores as low as 550–580 through manual underwriting, provided the borrower has strong residual income and a stable 12-month paymeRead more

The VA does not have a minimum credit score requirement, but most private lenders require a minimum FICO score of 620. Some specialized lenders may approve VA loans with scores as low as 550–580 through manual underwriting, provided the borrower has strong residual income and a stable 12-month payment history. For the best interest rates in 2026, a credit score of 720 or above is recommended.

See lessWhen I was going through the process last year, I was stressed about my 610 score, but I learned that the "minimum score" is actually a bit of a moving target. The VA itself is incredibly flexible because its goal is to help us get into homes. They don't mandate a specific credit floor. The catch isRead more

When I was going through the process last year, I was stressed about my 610 score, but I learned that the “minimum score” is actually a bit of a moving target. The VA itself is incredibly flexible because its goal is to help us get into homes. They don’t mandate a specific credit floor.

See lessThe catch is what the industry calls “lender overlays.” Basically, because the lender is taking the initial risk, they add their own rules on top of the VA’s guidelines. For most big banks, 620 is the “magic number” for a smooth approval. If you’re above that, you’ll likely breeze through the automated systems.

If you’re sitting between 550 and 600, you aren’t necessarily out of the running, but you’ll probably face manual underwriting. This is where a human being actually looks at your whole life story—your job stability, how much “residual income” you have left after bills, and why your score is what it is.

In the current 2026 market, with rates hovering around 6%, having a score above 720 will definitely snag you a much better interest rate, which can save you hundreds a month. My advice? Shop around! One lender might say no at 580, while another who specialises in VA loans will say yes.