Latest News & Updates

QNAPANDIT Latest Articles

The Ultimate Guide to Crafting AI Prompts That Work

Good AI prompts can make or break your results, but most people waste time on prompting “hacks” that don’t actually work. This guide is for anyone using AI tools like ChatGPT, Claude, or other language models who wants to get better outputs without falling for the latest prompt influencer trends. You’ll learn practical techniques that […]

The Ultimate Guide to Cybersecurity for Small Businesses

Small business owners face a growing number of cyber threats that can devastate operations, finances, and reputation. This comprehensive guide is designed for entrepreneurs, small business owners, and team leaders who need practical cybersecurity solutions without breaking the bank or requiring technical expertise. Cybercriminals increasingly target small businesses because they often lack robust security measures. […]

Fixed vs. Growth Mindset: Which One Wins?

Your mindset shapes everything—from how you handle setbacks to whether you even try new things. This deep dive is for entrepreneurs, business leaders, and anyone curious about growth mindset vs fixed mindset psychology who wants to understand which approach actually drives success. Many people believe talent and intelligence are set in stone. But research shows […]

How to Write a Business Plan (India, 2026): Step-by-Step

Starting a business in India has never been more accessible, but turning your idea into reality still requires a solid plan. This comprehensive guide shows you how to write a business plan that actually works for Indian entrepreneurs in 2026. This step-by-step business plan guide is designed for first-time entrepreneurs, startup founders, and small business […]

7 AI Myths That Are Holding Your Business Back

AI myths are stopping small and medium businesses from tapping into artificial intelligence’s real potential. These misconceptions spread faster than facts, leaving business owners convinced that AI is either too complex, too expensive, or too risky for their operations. This article is for business owners, managers, and decision-makers who want to separate AI reality from […]

10 Lifestyle Changes That Boost Focus Instantly

Struggling to concentrate at work, during studies, or while tackling daily tasks? We’ve all been there – staring at our computers while our minds wander, or reading the same paragraph three times without absorbing a word. The good news is that small lifestyle changes for better focus can make a dramatic difference in how well […]

The Shocking Truth About Home Yoga That Studios Don’t Want You to Know

Studios charge premium prices for what we can achieve right in our living rooms – and the home yoga benefits often surpass traditional classes. This guide is for busy people who want to start yoga at home, for beginners, experienced practitioners seeking flexibility, and anyone tired of expensive studio memberships that don’t fit their schedule. […]

The Ultimate Guide to Understanding Monthly Credit Score Swings

Your credit score doesn’t stay the same from month to month, and those monthly credit score changes can feel confusing and stressful. This comprehensive guide breaks down everything you need to know about credit score fluctuations and helps you take control of your financial health. Who this guide is for: Anyone who’s noticed their credit […]

Why Closing Old Credit Cards Could Destroy Your Score

Closing old credit cards can tank your credit score in ways most people don’t expect. This guide is for anyone considering cancelling old cards, whether you’re decluttering your wallet or avoiding annual fees. Your credit score takes a hit primarily because closing credit cards affects your credit utilisation ratio. When you lose that available credit […]

Crypto Portfolio Strategy 2026: Safe Diversification in INR

Building a smart crypto portfolio in 2026 means more than just buying Bitcoin and hoping for the best. With institutional money pouring into crypto ETFs and new asset classes like tokenised real estate hitting the scene, Indian investors need a structured approach to spread risk across this volatile market while keeping their rupee investments safe. […]

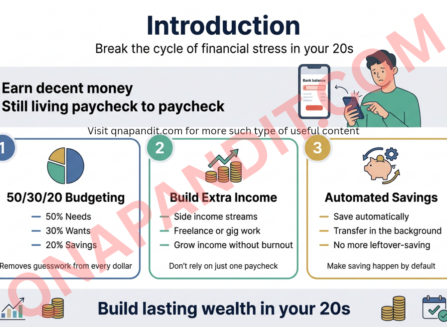

Why 99% of People in Their 20s Never Build Wealth (And How to Be the 1%)

Most twenty-somethings earn decent money but still live paycheck to paycheck. They watch their bank account hover near zero while wondering why wealth building in their 20s feels impossible for them, but easy for others. This guide is for young adults who want to break the cycle of financial stress and join the small group […]

Emergency Fund India 2026: How Much You Really Need (Calculator Included)

Life throws curveballs—job loss, medical emergencies, urgent repairs—and most Indians aren’t financially prepared for them. Without an emergency fund, you’ll end up using credit cards at 36-42% interest or selling investments at a loss when you need money the most. This guide is for working professionals, freelancers, and business owners who want to build a […]

Don’t Use ChatGPT Until You Try This Money Trick

Most entrepreneurs chase ChatGPT money-making tricks but end up with nothing to show for their efforts. This guide is for business owners and side hustlers who want to actually profit from AI instead of just collecting screenshots and hoping for the best. ChatGPT won’t magically print money. The real opportunity lies in using AI business […]

This ONE Legal Trick Boosted My Credit Score 200 Points in 30 Days!

Your credit score is tanking and you need results fast. Maybe you’re trying to qualify for a mortgage, get approved for that car loan, or finally move into your dream apartment. Whatever your reason, you’re not alone – millions of Americans struggle with low credit scores that block them from financial opportunities. This guide is […]

Freelancer’s Guide to Starting a One-Person Business (2026 Blueprint)

Ready to ditch the 9-to-5 and build something that’s truly yours? This freelancer’s guide to starting a one-person business shows you exactly how to transform your skills into a profitable solo venture in 2026. This blueprint is designed for ambitious freelancers, side hustlers looking to go full-time, and anyone who wants to escape the traditional […]

The Ultimate Guide to Boosting Your Credit Score in 90 Days

A poor credit score can cost you thousands of dollars in higher interest rates and limit your access to loans, apartments, and even some jobs. If you’re dealing with bad credit from past mistakes, preparing for a major purchase, or simply want to improve your financial standing, this 90-day credit improvement plan can help you […]

Local SEO for Indian SMBs: Step-by-Step Optimisation

Getting found online shouldn’t feel impossible for small business owners in India. When someone searches “dentist near me” or “best restaurant in Koramangala,” your business deserves to show up first – not buried on page two where nobody looks. Local SEO for Indian SMBs is your roadmap to dominating search results in your area. This […]

Why PAA Questions Are SEO Gold (And How to Mine Them)

Google’s People Also Ask boxes appear in over 43% of search results, yet most marketers ignore this goldmine of SEO opportunities. PAA questions reveal exactly what your audience wants to know, giving you a direct path to featured snippets, voice search optimization, and higher rankings. This guide is for content marketers, SEO specialists, and business […]

How to Start Crypto Staking in India: Earn Passive Crypto Income

Crypto staking lets you earn passive income from your digital assets while supporting blockchain networks. If you’re an Indian crypto investor looking to generate steady returns without active trading, staking offers a compelling opportunity to put your cryptocurrency to work. This guide is designed for beginners who want to start earning crypto staking rewards in […]

5 Crypto Investing Mistakes and How to Avoid Them

Cryptocurrency investing in India is growing rapidly, but many new investors make costly mistakes that could have been avoided with better preparation. This guide is designed for beginners and intermediate investors who want to build a profitable crypto portfolio while staying safe and compliant with Indian regulations. New crypto investors often lose money because they […]

How to attract and retain top Salesforce developer talent

The Salesforce talent market is red-hot, and finding skilled developers is just half the battle. The real challenge? Keeping them on your team once you’ve hired them. This guide is for hiring managers, HR leaders, and team leads who want to build and maintain high-performing Salesforce development teams. With developer demand far outpacing supply, your […]

Why Most Bloggers Ignore PAA (And Miss 40% More Traffic)

Most bloggers are leaving serious money on the table by ignoring one of Google’s most visible features. If you’re a content creator, digital marketer, or business owner struggling to increase organic traffic despite publishing consistently, you’re not alone. Over 80% of blogs fail within 18 months, and one major reason is overlooking People Also Ask […]

2026 Global Economic Outlook: Recession Risks, AI Boosts, and Smart Money Moves for USA, Canada, Australia

The 2026 global economic outlook presents a fascinating mix of AI-driven opportunities and traditional recession risks that smart investors need to navigate carefully. This comprehensive analysis is designed for investors, financial advisors, and business leaders in the USA, Canada, and Australia who want to understand how artificial intelligence, shifting monetary policies, and structural market changes […]

How to Turn Your Hobby Into a Profitable Career Skill

Your hobby feels more like an escape from work than just a weekend activity. We get it—that creative spark or hands-on satisfaction you find in photography, cooking, woodworking, or whatever gets you excited might actually be pointing toward your next career move. This guide is for anyone tired of watching the clock at their day […]

The Ultimate SEO Toolkit: 5 Must-Have Tools for 2026

SEO success in 2026 demands more than traditional keyword stuffing and link building. You need tools that can navigate AI-powered search engines, track your brand’s visibility in ChatGPT responses, and optimise for Google’s AI Overviews alongside classic organic rankings. This guide is designed for digital marketers, content creators, SEO professionals, and business owners who want […]

How to Choose a Domain When Your Perfect Name Is Taken

How to Choose a Domain When Your Perfect Name Is Taken Finding out your dream domain name taken can feel like a punch to the gut. You’ve brainstormed the perfect name for your business or blog, only to discover someone else got there first. This guide is for entrepreneurs, bloggers, and anyone launching a website […]

Erotica AI: Advancing Adult Fiction in the Digital Age

Artificial intelligence is steadily transforming creative industries, and one of its more specialised directions is erotica AI. Built on sophisticated language models, this technology can generate romantic and adult-themed stories from simple prompts. Instead of replacing authors, erotica AI serves as a creative assistant, helping users shape ideas, organise plots, and develop compelling characters with […]

How much should I save for retirement in my 20s?

Saving for retirement in your 20s is a smart financial move that can set you up for a comfortable future. Here's a guide on how much you should save: 1. Start Early: Time is your biggest asset when saving for retirement due to the power of compounding interest. The earlier you start, the less you'llRead more

Saving for retirement in your 20s is a smart financial move that can set you up for a comfortable future. Here’s a guide on how much you should save:

1. Start Early: Time is your biggest asset when saving for retirement due to the power of compounding interest. The earlier you start, the less you’ll have to save each month to reach your goal.

2. Set a Target: Financial experts often recommend saving between 10% to 15% of your income for retirement. However, everyone’s situation is unique so adjust this percentage based on your income, expenses, and retirement goals.

3. Consider Matching Contributions: If your employer offers a retirement savings plan like a 401(k) with a matching contribution, try to contribute enough to get the full match. It’s essentially free money and boosts your retirement savings significantly.

4. Use Retirement Calculators: Online retirement calculators can help you estimate how much you should save based on factors like your age, income, current savings, and retirement age. This can give you a clearer picture of your retirement savings goal.

5. Increase Savings with Income Growth: As your income grows throughout your career, aim to increase your retirement savings contributions. This will help you stay on track to reach your retirement savings goal.

6. Monitor and Adjust: Regularly review your retirement savings progress and be prepared to adjust your contributions if needed. Life circumstances change, so it’s important to stay flexible with your savings

See lessWhat are the common budgeting mistakes to avoid?

Common budgeting mistakes to avoid include: 1. Not Creating a Detailed Budget: Failing to establish a comprehensive budget can lead to overspending, missed savings opportunities, and financial insecurity. 2. Underestimating Expenses: Many people only consider fixed expenses like rent or mortgage payRead more

Common budgeting mistakes to avoid include:

1. Not Creating a Detailed Budget: Failing to establish a comprehensive budget can lead to overspending, missed savings opportunities, and financial insecurity.

2. Underestimating Expenses: Many people only consider fixed expenses like rent or mortgage payments, but forget about irregular expenses like car repairs or medical bills. It’s crucial to account for all potential expenses.

3. Ignoring Emergency Funds: Not setting aside money for unexpected emergencies can derail your financial goals when unforeseen expenses arise.

4. Failing to Track Spending: Without monitoring your expenses regularly, it’s easy to lose control of your budget. Tracking your spending helps identify areas where you can cut back or save more.

5. Relying on Credit Cards: Depending on credit cards to cover budget shortfalls can lead to high-interest debt that becomes difficult to pay off, creating a cycle of financial stress.

6. Overlooking Small Expenses: While small purchases may seem insignificant, they can add up over time and sabotage your budget. Being mindful of even minor expenses is essential for staying on track.

7. Not Reviewing and Adjusting Your Budget: Circumstances change, so it’s essential to regularly review your budget and make necessary adjustments to ensure it aligns with your financial goals.

8. Forgetting Long-term Financial Planning: Focusing solely on immediate financial needs without considering long-term goals like retirement savings or investments can hinder your overall financial well-being.

It’s

See lessHow to budget for irregular income?

Budgeting for irregular income can be challenging, but with the right strategies, you can effectively manage your finances. Here are some expert tips to help you budget for irregular income: 1. Calculate Your Average Monthly Income:- Review your income from the past year or more to determine an averRead more

Budgeting for irregular income can be challenging, but with the right strategies, you can effectively manage your finances. Here are some expert tips to help you budget for irregular income:

1. Calculate Your Average Monthly Income:

– Review your income from the past year or more to determine an average monthly income. This will give you a baseline to work with.

2. Create a Bare-Bones Budget:

– Identify essential expenses like housing, utilities, groceries, and transportation. Allocate funds to cover these necessities first.

3. Build an Emergency Fund:

– Set aside money from your irregular income to create an emergency fund that can cover unexpected expenses or income gaps.

4. Prioritize Savings Goals:

– Determine your financial goals such as debt repayment, retirement savings, or a major purchase. Allocate a portion of your income to each goal.

5. Use a Zero-Sum Budget Approach:

– Give every dollar a job by assigning specific categories for spending, saving, and investing. Adjust your budget as your income varies.

6. Track Your Spending:

– Keep a close eye on your expenses to ensure you’re staying within your budget. Use budgeting tools or apps to help you track your financial transactions.

7. Adjust Your Budget Regularly:

– Since your income fluctuates, it’s important to review and adjust your budget on a regular basis. Be flexible and adaptable to changes in your financial situation.

8

See lessCan I save money without cutting my lifestyle drastically?

Yes, it is possible to save money without drastically cutting your lifestyle by implementing some smart strategies and making conscious decisions. Here's how you can do it: 1. Budgeting: Create a detailed budget to track your income and expenses. Identify areas where you can cut back without signifiRead more

Yes, it is possible to save money without drastically cutting your lifestyle by implementing some smart strategies and making conscious decisions. Here’s how you can do it:

1. Budgeting: Create a detailed budget to track your income and expenses. Identify areas where you can cut back without significantly impacting your lifestyle.

2. Reduce Unnecessary Expenses: Review your spending habits and identify items or services you can live without. Cut back on dining out, subscription services, or impulse purchases.

3. Prioritize Savings: Treat savings like a recurring expense. Set up automated transfers to your savings account each month before you spend on non-essentials.

4. Comparison Shopping: Compare prices before making significant purchases. Look for discounts, coupons, and deals to save money without sacrificing quality.

5. Meal Planning: Plan your meals ahead to avoid wastage and unnecessary trips to the grocery store. Cook at home more often to save on dining expenses.

6. Seek Discounts and Rewards: Take advantage of loyalty programs, cashback rewards, and discounts offered by retailers to save money on everyday purchases.

7. Review Subscriptions: Identify and cancel any unused or unnecessary subscriptions like gym memberships, streaming services, or magazine subscriptions.

8. Energy Efficiency: Save on utility bills by being mindful of energy consumption. Turn off lights and unplug devices when not in use, and consider energy-efficient appliances.

By implementing these practical tips, you can start saving money without drastically altering your lifestyle. Remember,

See lessHow many goldbees is 1 gram of gold?

One gram of gold is approximately equivalent to 62.2 "goldbees."- "Goldbee" is a fictional term not recognized in the standard units of measurement.- The question seems to be a play on words or a made-up concept rather than based on factual information.- Gold weight is typically measured in grams, oRead more

One gram of gold is approximately equivalent to 62.2 “goldbees.”

– “Goldbee” is a fictional term not recognized in the standard units of measurement.

– The question seems to be a play on words or a made-up concept rather than based on factual information.

– Gold weight is typically measured in grams, ounces, or troy ounces, not in unconventional units like “goldbees.”

– To determine the amount of gold in grams, you can use a precise weighing scale designed for small weights.

Hope this helps—feel free to add your experience or ask a follow-up.

See lessHow do I create an emergency fund from scratch?

Creating an emergency fund from scratch is a crucial step in achieving financial stability and peace of mind. Here's a detailed guide on how to build an emergency fund effectively:Step 1: Set a Clear Goal- Determine how much you want to save for your emergency fund. A common recommendation is to havRead more

Creating an emergency fund from scratch is a crucial step in achieving financial stability and peace of mind. Here’s a detailed guide on how to build an emergency fund effectively:

Step 1: Set a Clear Goal

– Determine how much you want to save for your emergency fund. A common recommendation is to have 3 to 6 months’ worth of living expenses.

Step 2: Track Your Expenses

– Analyze your monthly expenses to understand your spending habits and identify areas where you can cut back to save more.

Step 3: Create a Budget

– Develop a realistic budget that allocates a portion of your income towards your emergency fund. Consider using budgeting tools or apps to help you stay on track.

Step 4: Start Small and Be Consistent

– Begin by setting achievable savings goals. Even saving a small amount regularly can add up over time. Consistency is key.

Step 5: Choose the Right Savings Account

– Opt for a high-yield savings account or a money market account that offers competitive interest rates to help your money grow faster.

Step 6: Automate Your Savings

– Set up automatic transfers from your checking account to your emergency fund to ensure a consistent savings habit.

Step 7: Reassess and Adjust

– Periodically review your budget and savings goals. Adjust as needed based on changes in your income or expenses.

Common Mistakes to Avoid:

– Not Prioritizing Emergency Fund:

See lessIs the 50/30/20 budgeting rule effective?

The 50/30/20 budgeting rule, popularized by Senator Elizabeth Warren in her book "All Your Worth: The Ultimate Lifetime Money Plan," is a simple and effective guideline for managing personal finances. Here's an overview of the rule's effectiveness and some key points to consider:What is the 50/30/20Read more

The 50/30/20 budgeting rule, popularized by Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan,” is a simple and effective guideline for managing personal finances. Here’s an overview of the rule’s effectiveness and some key points to consider:

What is the 50/30/20 Budgeting Rule?

1. 50% Needs, 30% Wants, 20% Savings/Debt Repayment:

– Allocate 50% of your after-tax income to necessities like housing, utilities, food.

– Dedicate 30% to discretionary expenses such as dining out, shopping, entertainment.

– Save 20% for financial goals like emergency fund, retirement savings, debt payments.

Effectiveness of the Rule:

1. Simplicity and Clarity:

– Easy-to-understand framework for budgeting.

– Provides a balanced approach to managing finances.

2. Promotes Financial Health:

– Encourages saving and debt reduction.

– Helps prioritize spending on essentials over wants.

3. Personalization:

– Can be adjusted based on individual circumstances.

– Serves as a foundation for building a more detailed budget.

Hidden Pain Points and Considerations:

1. Variability:

– Fixed living costs may exceed 50%, especially in high-cost areas.

– Personal situations might require flexibility in the allocation percentages.

2. **Emergency Fund

See less