Latest News & Updates

QNAPANDIT Latest Articles

The AI Gold Rush Is Here: 6 Simple Ways Beginners Are Banking $10K+ Monthly in 2026

The AI gold rush isn’t coming—it’s already here. Right now, thousands of beginners are using simple AI tools to generate serious monthly income, with many breaking the $10K barrier faster than anyone expected. This guide is for complete beginners who want practical, proven strategies to make money with AI in 2026. You don’t need coding […]

How to Start Crypto Staking in India: Earn Passive Crypto Income

Crypto staking lets you earn passive income from your digital assets while supporting blockchain networks. If you’re an Indian crypto investor looking to generate steady returns without active trading, staking offers a compelling opportunity to put your cryptocurrency to work. This guide is designed for beginners who want to start earning crypto staking rewards in […]

The Ultimate Guide to Understanding Monthly Credit Score Swings

Your credit score doesn’t stay the same from month to month, and those monthly credit score changes can feel confusing and stressful. This comprehensive guide breaks down everything you need to know about credit score fluctuations and helps you take control of your financial health. Who this guide is for: Anyone who’s noticed their credit […]

Best Side Hustles to Make Money Online in 2026

The internet has completely transformed the way people earn money. What started as freelancing and blogging years ago has evolved into a massive digital economy filled with opportunities for creators, freelancers, entrepreneurs, students, remote workers, and even complete beginners. In 2026, side hustles are no longer just “extra income” ideas. For many people, they’ve become […]

2026 Budget Planner for Beginners: Zero-Based Budgeting Guide

Ready to take control of your money in 2026? Zero-based budgeting might be exactly what you need to finally see where every dollar goes. This 2026 budget planner for beginners will show you how zero-based budgeting works – a simple method where your income minus expenses equals zero every month. Don’t worry, that doesn’t mean […]

What Is Credit Utilization? (And Why It Matters)

Your credit score can make or break major financial decisions, and credit utilisation plays a bigger role than most people realise. If you’re wondering what credit utilisation is and why it matters so much to lenders, you’re not alone—many people don’t fully understand how this simple percentage affects their borrowing power. This guide is for […]

Gmail AI vs. Outlook AI: Which Assistant Wins?

AI email assistants have gone from tech novelty to daily necessity, but choosing between Gmail AI vs Outlook AI feels overwhelming when you’re drowning in messages. This guide is for busy professionals, small business owners, and anyone who processes 50+ emails daily and wants to reclaim their time without switching their entire workflow. Smart email […]

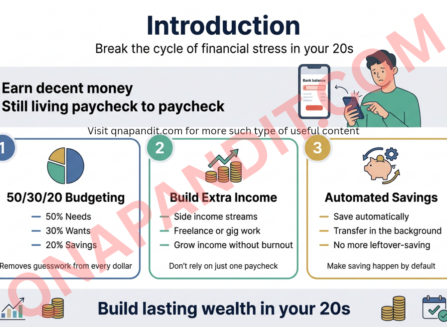

Why 99% of People in Their 20s Never Build Wealth (And How to Be the 1%)

Most twenty-somethings earn decent money but still live paycheck to paycheck. They watch their bank account hover near zero while wondering why wealth building in their 20s feels impossible for them, but easy for others. This guide is for young adults who want to break the cycle of financial stress and join the small group […]

Timur Turlov and the Global Development of Freedom Holding

In recent years, financial entrepreneur Timur Turlov has attracted attention in the global finance sector as the founder and CEO of Freedom Holding Corp. As financial markets become more interconnected and technology reshapes how investors access global exchanges, companies like Freedom Holding represent a broader shift toward modern, digital-driven financial services. Freedom Holding Corp. operates […]

Building Your First Team: Hiring for Your Small Business

Hiring your first employee marks a major milestone for any small business owner. You’re moving from a one-person operation to building a real team—and that’s both exciting and scary. This guide is for small business owners and entrepreneurs ready to make their first hires or expand their existing teams. We’ll walk you through everything from […]

The Ultimate Guide to Cybersecurity for Small Businesses

Small business owners face a growing number of cyber threats that can devastate operations, finances, and reputation. This comprehensive guide is designed for entrepreneurs, small business owners, and team leaders who need practical cybersecurity solutions without breaking the bank or requiring technical expertise. Cybercriminals increasingly target small businesses because they often lack robust security measures. […]

10 Online Business Ideas Under ₹50,000 (India, 2026 Edition)

Starting an online business in India doesn’t need to break your bank account. With just ₹50,000, you can launch a profitable venture from your home and tap into India’s booming digital economy. This guide is perfect for college students, working professionals seeking side income, and aspiring entrepreneurs who want to start small and scale smartly. […]

7 Tech Trends That Will Transform Your Life by 2030

Technology is advancing faster than ever, and by 2030, several breakthrough innovations will completely change how you live, work, and interact with the world around you. This guide is for tech enthusiasts, business professionals, and anyone curious about the future who wants to understand which emerging technologies will have the biggest impact on daily life. […]

99% of Indians Don’t Know These 7 Passive Income Secrets That Actually Work in 2026

Most Indians work hard but stay financially stressed because they rely on just one income source. The traditional advice of “save more, spend less” only gets you so far when your salary barely keeps up with rising costs. The passive income secrets that actually work in 2026 aren’t the typical “make money while you sleep” […]

7 Proven Ways to Make Real Money Online in 2026 and beyond

Making money online in 2026 isn’t about overnight riches or shiny get-rich-quick schemes. The real opportunities exist for people who want sustainable income streams they can actually count on. This guide is for anyone tired of the hype – freelancers looking to diversify their income, professionals wanting to build passive revenue, or entrepreneurs ready to […]

Crypto Portfolio Strategy 2026: Safe Diversification in INR

Building a smart crypto portfolio in 2026 means more than just buying Bitcoin and hoping for the best. With institutional money pouring into crypto ETFs and new asset classes like tokenised real estate hitting the scene, Indian investors need a structured approach to spread risk across this volatile market while keeping their rupee investments safe. […]

10 Lifestyle Changes That Boost Focus Instantly

Struggling to concentrate at work, during studies, or while tackling daily tasks? We’ve all been there – staring at our computers while our minds wander, or reading the same paragraph three times without absorbing a word. The good news is that small lifestyle changes for better focus can make a dramatic difference in how well […]

Transforming the Educational Landscape: The Value of an Education Franchise in Nigeria

The global demand for high-quality supplementary learning has witnessed a dramatic surge over recent years. In rapidly developing economies, traditional academic structures face massive challenges trying to keep pace with the cognitive and technological skills required for the modern global workforce. As a result, parents are increasingly looking for specialized programs that go beyond basic […]

The Ultimate SEO Toolkit: 5 Must-Have Tools for 2026

SEO success in 2026 demands more than traditional keyword stuffing and link building. You need tools that can navigate AI-powered search engines, track your brand’s visibility in ChatGPT responses, and optimise for Google’s AI Overviews alongside classic organic rankings. This guide is designed for digital marketers, content creators, SEO professionals, and business owners who want […]

5 Morning Habits That Boost Energy Without Coffee

Tired of depending on coffee to jumpstart your day? You’re not alone. Many people struggle with low energy in the morning and wonder how to wake up energised without coffee. The good news is that simple, natural morning habits can boost energy levels just as effectively as your daily cup of joe. This guide is […]

Local SEO for Indian SMBs: Step-by-Step Optimisation

Getting found online shouldn’t feel impossible for small business owners in India. When someone searches “dentist near me” or “best restaurant in Koramangala,” your business deserves to show up first – not buried on page two where nobody looks. Local SEO for Indian SMBs is your roadmap to dominating search results in your area. This […]

Social Media Marketing on a Budget: Small Biz Strategies

Small business owners know they need a strong social media presence, but many worry about the costs. The truth is, you don’t need a massive marketing budget to succeed on social platforms. Smart small business social media strategies can deliver real results without breaking the bank. This guide is for small business owners, entrepreneurs, and […]

7 AI Myths That Are Holding Your Business Back

AI myths are stopping small and medium businesses from tapping into artificial intelligence’s real potential. These misconceptions spread faster than facts, leaving business owners convinced that AI is either too complex, too expensive, or too risky for their operations. This article is for business owners, managers, and decision-makers who want to separate AI reality from […]

Don’t Use ChatGPT Until You Try This Money Trick

Most entrepreneurs chase ChatGPT money-making tricks but end up with nothing to show for their efforts. This guide is for business owners and side hustlers who want to actually profit from AI instead of just collecting screenshots and hoping for the best. ChatGPT won’t magically print money. The real opportunity lies in using AI business […]

This ONE Legal Trick Boosted My Credit Score 200 Points in 30 Days!

Your credit score is tanking and you need results fast. Maybe you’re trying to qualify for a mortgage, get approved for that car loan, or finally move into your dream apartment. Whatever your reason, you’re not alone – millions of Americans struggle with low credit scores that block them from financial opportunities. This guide is […]

Why PAA Questions Are SEO Gold (And How to Mine Them)

Google’s People Also Ask boxes appear in over 43% of search results, yet most marketers ignore this goldmine of SEO opportunities. PAA questions reveal exactly what your audience wants to know, giving you a direct path to featured snippets, voice search optimization, and higher rankings. This guide is for content marketers, SEO specialists, and business […]

How to Write a Business Plan (India, 2026): Step-by-Step

Starting a business in India has never been more accessible, but turning your idea into reality still requires a solid plan. This comprehensive guide shows you how to write a business plan that actually works for Indian entrepreneurs in 2026. This step-by-step business plan guide is designed for first-time entrepreneurs, startup founders, and small business […]

How to Choose a Profitable Niche for blogging in 2026

Finding Your Perfect Profitable Blogging Niche for 2026: A Strategic Guide Choosing the right blogging niche can make or break your online success. Many new bloggers jump in without research, only to discover their topic has no audience or money-making potential. This guide is for aspiring bloggers, content creators switching niches, and anyone wanting to […]

How to Rebuild Your CIBIL Score After Settlement in 6 Months

Settled a loan and watching your CIBIL score plummet? You’re not alone. Thousands of borrowers face the same challenge after choosing settlement over prolonged EMI struggles, but the good news is that CIBIL score improvement after settlement is absolutely possible with the right approach. This guide is for anyone who has recently settled a loan […]

step-by-step zero-based budget creation process

Creating a zero-based budget involves a meticulous process that ensures every dollar you earn has a designated purpose. Here is a step-by-step guide to help you through the zero-based budget creation process: 1. Gather Financial Information:- Collect all sources of income.- Compile a list of all expRead more

Creating a zero-based budget involves a meticulous process that ensures every dollar you earn has a designated purpose. Here is a step-by-step guide to help you through the zero-based budget creation process:

1. Gather Financial Information:

– Collect all sources of income.

– Compile a list of all expenses, including fixed, variable, and occasional expenses.

2. Track Your Spending:

– Monitor your expenses for a month to understand your spending patterns.

– Categorize your expenses (e.g., housing, utilities, groceries, entertainment) for better clarity.

3. Calculate Your Income:

– Determine your total monthly income after taxes.

– Take into account any additional or irregular income sources.

4. List Your Expenses:

– Create a comprehensive list of all your expenses.

– Differentiate between needs (essential expenses) and wants (discretionary spending).

5. Assign Every Dollar a Job:

– Start allocating your income to cover each expense category.

– Ensure that your total expenses match your total income, leaving no money unassigned.

6. Adjust and Refine:

– Fine-tune your budget by adjusting spending in certain categories.

– Consider cutting back on non-essential expenses to align your budget with your financial goals.

7. Monitor and Review:

– Regularly track your expenses to ensure you are sticking to your budget.

– Review your budget monthly and make necessary

See lesshow to prioritise your essential categories and budget allocation?

Prioritizing essential categories and budget allocation is crucial for effective financial management. Here’s a comprehensive guide to help you navigate this process successfully: 1. Assess Your Financial Situation:- Start by evaluating your current financial status, including income, expenses, debtRead more

Prioritizing essential categories and budget allocation is crucial for effective financial management. Here’s a comprehensive guide to help you navigate this process successfully:

1. Assess Your Financial Situation:

– Start by evaluating your current financial status, including income, expenses, debts, savings, and financial goals.

– Understand your spending patterns to identify essential categories where you need to allocate funds.

2. Identify Your Essential Categories:

– Categorize your expenses into essential (needs) and non-essential (wants) categories.

– Essential categories typically include housing, utilities, groceries, transportation, debt payments, insurance, and healthcare.

3. Establish Priorities:

– Rank your essential categories based on their importance and impact on your daily life and financial well-being.

– Allocate a higher percentage of your budget to vital categories like housing, groceries, and healthcare.

4. Create a Realistic Budget:

– Set specific budget limits for each essential category to ensure you allocate funds efficiently.

– Consider using the 50/30/20 rule where 50% of your income goes to needs, 30% to wants, and 20% to savings and debt repayment.

5. Monitor and Adjust Regularly:

– Track your expenses regularly to ensure you are sticking to your budget and adjusting as needed.

– Be flexible and make changes to your budget based on any fluctuations in income or expenses.

6. **Seek Professional

See lessRent vs Buy a home: which is better?

When deciding between renting and buying a home, there are several factors to consider to determine which option is better suited to your needs. Let's delve into the key aspects to help you make an informed decision:Renting a Home:* Pros:- greater flexibility to move without selling a property- loweRead more

When deciding between renting and buying a home, there are several factors to consider to determine which option is better suited to your needs. Let’s delve into the key aspects to help you make an informed decision:

Renting a Home:

* Pros:

– greater flexibility to move without selling a property

– lower upfront costs such as down payment and maintenance

– fewer responsibilities for repairs and maintenance

* Cons:

– lack of long-term investment potential

– limited control over changes to the property

– rent payments don’t build equity

Buying a Home:

* Pros:

– long-term investment potential through home equity

– stability and predictability of homeownership

– freedom to customize and make changes to the property

* Cons:

– higher upfront costs like down payment and closing costs

– responsibility for maintenance and repairs

– potential for property value fluctuations

Key Considerations:

1. Financial Considerations:

– Calculate the total costs of renting vs. buying, including mortgage payments, property taxes, insurance, and maintenance.

– Consider your financial stability, long-term goals, and local housing market trends.

2. Lifestyle and Flexibility:

– Evaluate how long you plan to stay in the home.

– Assess your lifestyle preferences for stability vs. flexibility.

3. Market Conditions:

– Research current real estate market conditions, interest rates, and trends.

–

See lessHow to build credit for beginners?

Building credit as a beginner is essential for establishing a strong financial foundation. Here are some steps to help you build credit effectively: 1. Open a credit card: Consider applying for a secured credit card or a beginner-friendly credit card to start establishing a credit history. Make smalRead more

Building credit as a beginner is essential for establishing a strong financial foundation. Here are some steps to help you build credit effectively:

1. Open a credit card: Consider applying for a secured credit card or a beginner-friendly credit card to start establishing a credit history. Make small purchases and pay off the balance in full each month to demonstrate responsible credit usage.

2. Become an authorized user: If someone you trust has a well-established credit card, ask if they can add you as an authorized user. This can help you piggyback off their good credit history and boost your own credit score.

3. Pay bills on time: Your payment history is a significant factor in your credit score. Make sure to pay all your bills, including credit card bills, loans, and utilities, on time each month.

4. Keep credit utilization low: Try to keep your credit card balances low in relation to your credit limit. Aim to use no more than 30% of your available credit to show that you can manage credit responsibly.

5. Monitor your credit report: Regularly check your credit report from the major credit bureaus (Equifax, Experian, TransUnion) to ensure all information is accurate. Report any errors or discrepancies promptly.

6. Apply for credit in moderation: Avoid applying for multiple credit accounts within a short period as it can negatively impact your credit score. Be strategic in your credit applications.

7. Consider a credit-builder loan: If you’re

See lessShould I refinance my mortgage?

Refinancing your mortgage is a significant financial decision that can have both short-term and long-term implications. To determine whether you should refinance your mortgage, consider the following key factors:Hidden User Pain Points: 1. Common Confusion: Understanding when it's the right time toRead more

Refinancing your mortgage is a significant financial decision that can have both short-term and long-term implications. To determine whether you should refinance your mortgage, consider the following key factors:

Hidden User Pain Points:

1. Common Confusion: Understanding when it’s the right time to refinance can be confusing for many homeowners. It’s essential to weigh the pros and cons carefully.

2. Mistakes: Some homeowners refinance without considering the total costs involved, including closing costs and potential prepayment penalties.

3. Risks: Refinancing may extend the term of your loan, which could result in paying more interest over time, even if you secure a lower interest rate.

4. Misconceptions: It’s a misconception that lowering your interest rate is always advantageous. If you don’t plan to stay in your home long enough to recoup the closing costs, refinancing may not be beneficial.

Factors to Consider:

See less1. Current Interest Rate: Compare your current interest rate with the current market rates to see if you could secure a lower rate through refinancing.

2. Financial Goals: Determine if your financial goals align with refinancing, whether it’s reducing monthly payments, paying off the loan faster, or accessing equity.

3. Break-Even Point: Calculate the break-even point to ensure that you’ll stay in the home long enough to benefit from the cost of refinancing.

4. Credit Score: A higher credit score often leads to better refinancing options, so consider your credit score

How much should I have in an emergency fund?

Having an emergency fund is crucial for financial stability and peace of mind. The general recommendation is to have 3 to 6 months' worth of living expenses saved up in an emergency fund. However, the ideal amount can vary based on individual circumstances, such as: 1. Monthly Expenses: Calculate yoRead more

Having an emergency fund is crucial for financial stability and peace of mind. The general recommendation is to have 3 to 6 months’ worth of living expenses saved up in an emergency fund. However, the ideal amount can vary based on individual circumstances, such as:

1. Monthly Expenses: Calculate your monthly expenses, including rent/mortgage, utilities, groceries, insurance, and debt payments.

2. Job Stability: If your job is stable, a smaller emergency fund may be sufficient. For those with irregular income or in high-risk industries, having a larger fund is advisable.

3. Dependents: If you have dependents or a family to support, a larger emergency fund provides a safety net for unexpected expenses.

4. Health Expenses: Individuals with chronic health conditions may want to save more to cover potential medical costs.

5. Debt Level: If you have high-interest debt, focusing on building a smaller emergency fund while paying off debt could be a sensible approach.

To calculate your specific emergency fund target, consider these factors and adjust the 3 to 6 months guideline accordingly. It’s also important to regularly review and adjust your emergency fund as your circumstances change.

Key Points to Consider:

– Begin by saving a starter fund of $1,000, then gradually build up to cover several months’ expenses.

– Keep your emergency fund in a separate, easily accessible account, such as a high-yield savings account.

– Only use the fund for true emergencies like medical expenses, car repairs,

See lessBest way to save for retirement in 2026?

Saving for retirement in 2026 requires careful planning and consideration to ensure a financially stable future. Here are some top strategies to help you save effectively: 1. Maximize Employer-Sponsored Retirement Accounts:- Contribute the maximum amount allowed to your 401(k) or 403(b) if your emplRead more

Saving for retirement in 2026 requires careful planning and consideration to ensure a financially stable future. Here are some top strategies to help you save effectively:

1. Maximize Employer-Sponsored Retirement Accounts:

– Contribute the maximum amount allowed to your 401(k) or 403(b) if your employer offers one.

– Take advantage of any employer matching contributions to boost your savings even further.

2. Consider Opening an IRA:

– Invest in a Traditional or Roth IRA to supplement your employer-sponsored retirement account.

– A Traditional IRA offers tax-deferred growth, while a Roth IRA provides tax-free withdrawals in retirement.

3. Diversify Your Investments:

– Spread your retirement savings across various asset classes to reduce risk and maximize returns.

– Consult with a financial advisor to create a diversified investment portfolio tailored to your risk tolerance and retirement goals.

4. Maintain a Budget and Cut Unnecessary Expenses:

– Track your expenses and identify areas where you can cut back to increase your retirement savings.

– Redirect the money saved from cutting expenses towards your retirement accounts.

5. Stay Informed and Adjust Your Plan:

– Regularly review your retirement savings plan and make adjustments as needed based on changing circumstances.

– Stay informed about retirement planning best practices and seek professional advice when necessary.

Remember, saving for retirement is a long-term endeavor that requires discipline and consistency. By starting early and following a strategic savings plan

See less