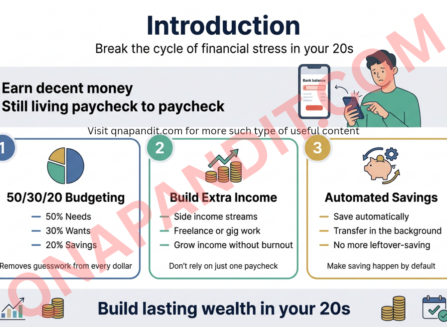

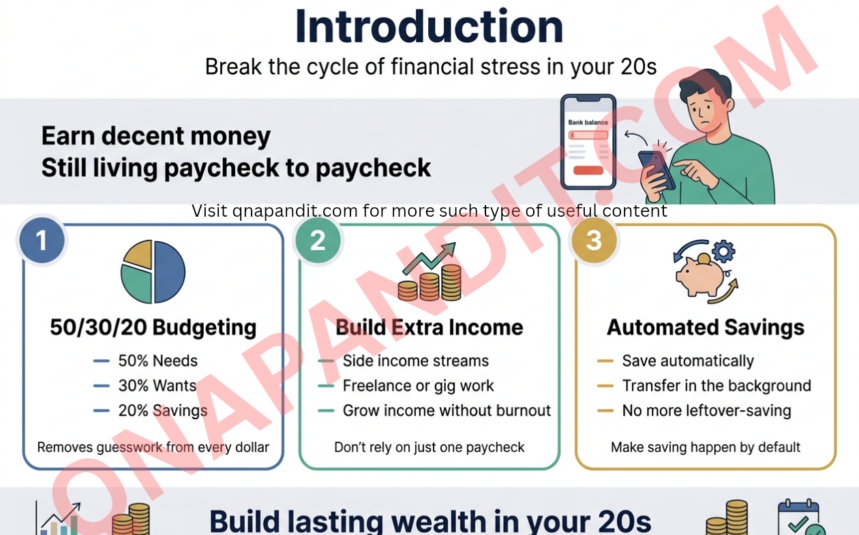

Most twenty-somethings earn decent money but still live paycheck to paycheck. They watch their bank account hover near zero while wondering why wealth building in their 20s feels impossible for them, but easy for others.

This guide is for young adults who want to break the cycle of financial stress and join the small group that actually builds lasting wealth during their twenties. If you’re tired of feeling behind financially while your peers seem to have it figured out, you’re in the right place.

We’ll cover the proven 50/30/20 budgeting system that removes guesswork from your money decisions and shows you exactly where every dollar should go. You’ll also learn practical strategies to generate additional income streams without burning yourself out – because relying on just your day job won’t cut it if you want real financial freedom.

Finally, we’ll set up automated savings strategies that work in the background while you live your life. No more hoping you’ll remember to save what’s left over at the end of the month.

Master the Foundation of Smart Money Management

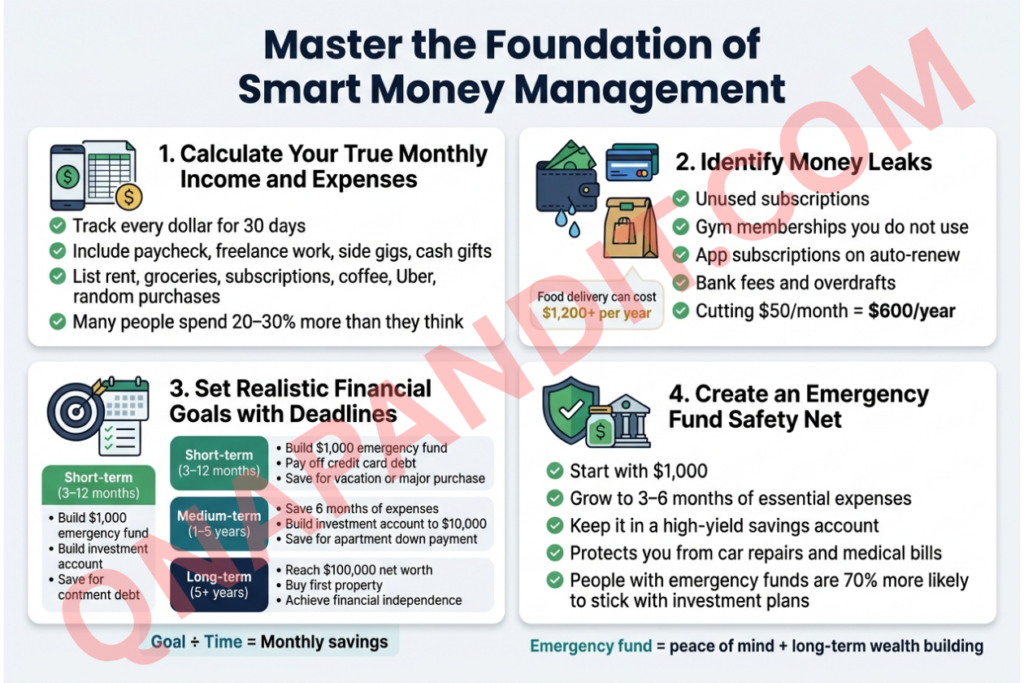

Calculate Your True Monthly Income and Expenses

Most people in their twenties have no clue how much money actually flows in and out of their accounts each month. This blind spot becomes the biggest roadblock to wealth building in 20s. Start by tracking every single dollar for at least 30 days using apps like Mint, YNAB, or even a simple spreadsheet.

Your true monthly income isn’t just your paycheck – include freelance work, side gigs, cash gifts, or any money that hits your account. For expenses, categorize everything: rent, groceries, subscriptions, coffee runs, Uber rides, and that random Amazon purchase you forgot about. The goal here is brutal honesty, not judgment.

Many young adults discover they’re spending 20-30% more than they thought once they see the real numbers. This awareness becomes your superpower for making smarter financial decisions.

Identify Money Leaks Draining Your Bank Account

Money leaks are those sneaky recurring expenses that quietly drain your wealth-building potential. The average person has $273 worth of unused subscriptions running each month. Check your bank statements for:

- Streaming services you never watch

- Gym memberships you don’t use

- App subscriptions on auto-renew

- Premium features you forgot about

- Bank fees for overdrafts or low balances

Money management tips for millennials always emphasize the power of small savings. Cutting just $50 monthly in subscriptions gives you $600 annually to invest. Over 10 years with compound growth, that becomes serious money.

Food delivery apps represent another massive leak. The average user spends $1,200+ yearly on delivery fees and markups. Cooking at home just three times per week instead of ordering saves hundreds monthly.

Set Realistic Financial Goals with Deadlines

Vague goals like “save more money” never work. Young adults financial planning requires specific, measurable targets with deadlines. Break your goals into three categories:

Short-term (3-12 months):

- Build $1,000 emergency fund

- Pay off credit card debt

- Save for a vacation or major purchase

Medium-term (1-5 years):

- Save 6 months of expenses

- Build investment account to $10,000

- Save for apartment down payment

Long-term (5+ years):

- Reach $100,000 net worth

- Buy first property

- Achieve financial independence

Write down exactly how much you need and when you want to achieve each goal. Then reverse-engineer the monthly savings required. If you want $5,000 saved in 10 months, you need to save $500 monthly. This clarity transforms wishful thinking into actionable plans.

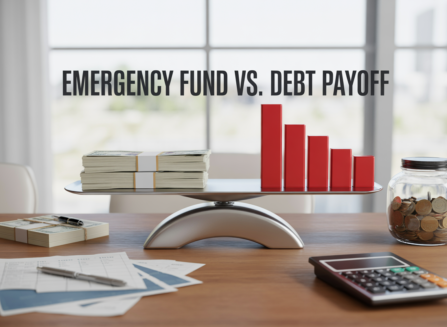

Create an Emergency Fund Safety Net

Your emergency fund protects your wealth-building journey from unexpected setbacks. Without one, a car repair or medical bill forces you to rack up credit card debt, destroying months of progress.

Start with $1,000 as your initial emergency fund – this covers most minor emergencies and builds the savings habit. Once you’ve mastered consistent saving, grow it to 3-6 months of essential expenses.

Keep this money in a high-yield savings account that’s separate from your checking account. You want it accessible but not so convenient that you’re tempted to dip into it for non-emergencies.

Personal finance for young professionals shows that people with emergency funds are 70% more likely to stick with their investment plans during market downturns. When your job security feels shaky or unexpected expenses hit, you’ll have breathing room to make rational decisions instead of panic moves that derail your financial future.

The emergency fund isn’t just about money – it’s about peace of mind that lets you take calculated risks and pursue opportunities that build long-term wealth.

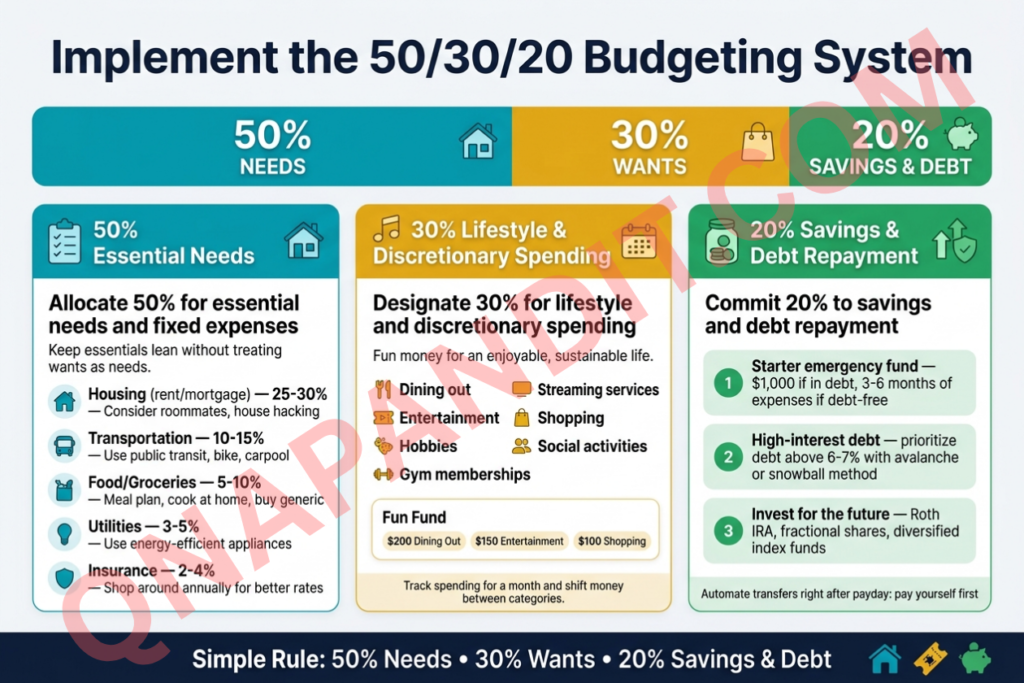

Implement the 50/30/20 Budgeting System

Allocate 50% for essential needs and fixed expenses

Your essential expenses eat up half your income, and that’s perfectly normal when you’re building wealth in your 20s. This 50% bucket covers your absolute must-haves: rent or mortgage payments, utilities, groceries, transportation costs, insurance premiums, and minimum debt payments. These are the expenses that keep your life running smoothly and can’t be easily eliminated.

The key lies in keeping this category lean without sacrificing your quality of life. Many young adults make the mistake of treating wants as needs, inflating this category beyond the recommended 50%. Consider your housing costs carefully – they’re typically your largest expense. If rent takes up more than 30% of your income, you might need to explore options like roommates, moving to a more affordable area, or house hacking strategies.

Transportation represents another major component. Before jumping into a hefty car payment, evaluate whether you truly need a vehicle or if public transportation, biking, or car-sharing services make more financial sense. Your grocery budget also falls here, but that doesn’t mean you need to survive on ramen. Smart shopping strategies like meal planning, buying generic brands, and cooking at home can keep this expense reasonable while maintaining good nutrition.

| Essential Expense Category | Typical Percentage of Income | Money-Saving Tips |

|---|---|---|

| Housing (rent/mortgage) | 25-30% | Consider roommates, house hacking |

| Transportation | 10-15% | Use public transit, bike, carpool |

| Food/Groceries | 5-10% | Meal plan, cook at home, buy generic |

| Utilities | 3-5% | Use energy-efficient appliances |

| Insurance | 2-4% | Shop around annually for better rates |

Designate 30% for lifestyle and discretionary spending

This 30% slice represents your fun money – the spending that makes life enjoyable and sustainable. Personal finance for young professionals shouldn’t feel like a punishment, and this category ensures you can maintain social connections and pursue interests without derailing your wealth-building goals.

Your discretionary spending includes dining out, entertainment, hobbies, gym memberships, streaming services, shopping for non-essential items, and social activities. The beauty of the 50/30/20 budget rule lies in its flexibility within this category. You get to decide what brings you the most joy and satisfaction.

Track your spending patterns for a month to understand where your discretionary money currently goes. You might discover you’re spending more on subscription services than you realize, or that impulse purchases are eating into funds you’d rather use for experiences. Money management tips for millennials often emphasize the importance of conscious spending rather than mindless restriction.

Consider implementing a “fun fund” approach within this 30%. Set aside specific amounts for different activities – maybe $200 for dining out, $150 for entertainment, and $100 for shopping. This method helps prevent overspending in one area while ensuring you don’t feel deprived in others. When you reach your limit in one category, you either wait until next month or shift money from another discretionary category.

Commit 20% to savings and debt repayment

The final 20% represents your ticket to financial freedom and long-term wealth building. This portion gets split between building your emergency fund, paying down high-interest debt, and investing for your future. How you divide this 20% depends on your current financial situation and goals.

Start by establishing a starter emergency fund of $1,000 if you’re dealing with debt, or aim for 3-6 months of expenses if you’re debt-free. This safety net prevents you from derailing your progress when unexpected expenses arise. Once your emergency fund reaches an appropriate level, redirect that money toward debt repayment or investments.

High-interest debt, particularly credit card debt, should be your top priority within this category. Any debt with an interest rate above 6-7% typically warrants aggressive payoff strategies. Use either the debt avalanche method (paying minimums on all debts while attacking the highest interest rate first) or the debt snowball method (starting with the smallest balance for psychological wins).

After handling emergency funds and high-interest debt, focus on building wealth through investing. Even small amounts make a significant difference when you’re in your twenties thanks to compound interest. Consider opening a Roth IRA and contributing consistently, even if you start with just $50 per month. Many brokerages offer fractional shares, making it easy to invest small amounts in diversified index funds.

Automated savings strategies work particularly well for this 20% allocation. Set up automatic transfers to separate savings and investment accounts right after payday. This “pay yourself first” approach removes the temptation to spend this money elsewhere and builds wealth-building habits that will serve you throughout your life.

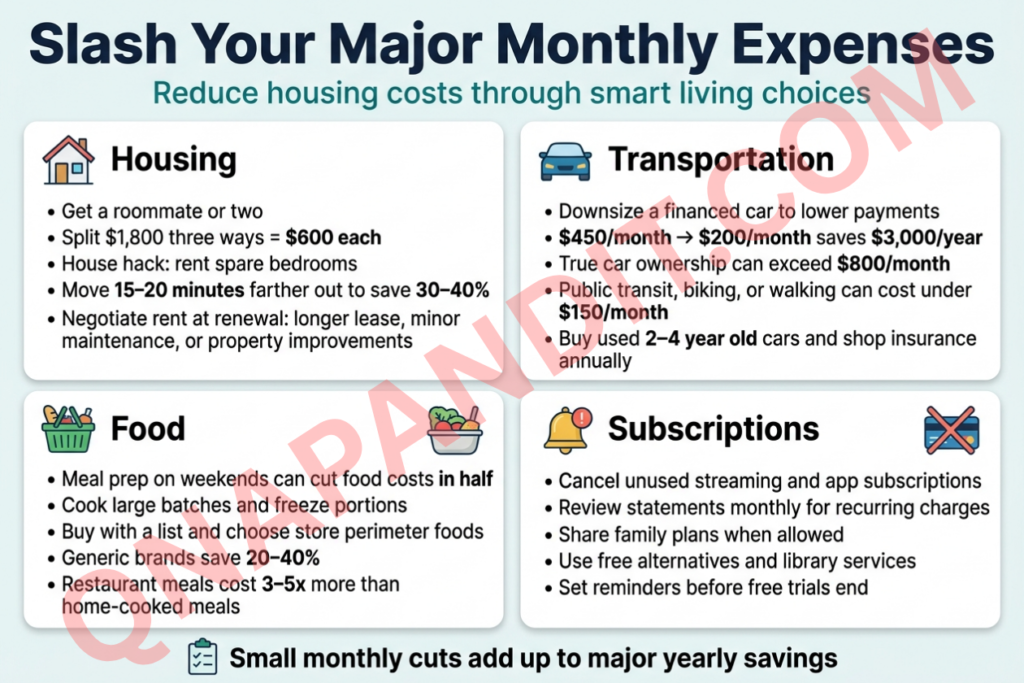

Slash Your Major Monthly Expenses

Reduce housing costs through smart living choices

Housing typically eats up the largest chunk of your income, but smart choices can save you thousands annually. Consider getting a roommate or two – splitting a $1,800 apartment three ways drops your share to $600 instead of paying $1,200 for a studio. House hacking presents another powerful strategy: rent out spare bedrooms in a property you own or find a landlord who’ll reduce your rent in exchange for property management duties.

Location flexibility opens massive savings opportunities. Moving just 15-20 minutes further from city centers often cuts rent by 30-40% while still maintaining reasonable commute times. Research up-and-coming neighborhoods before they become trendy – you’ll get better value and potential appreciation if you’re buying.

Negotiate with landlords, especially during lease renewals. Offer to sign longer terms, handle minor maintenance, or improve the property in exchange for reduced rent. Many landlords prefer reliable tenants over slightly higher rents.

Cut transportation expenses with strategic planning

Transportation costs drain wealth faster than most people realize. If you’re financing a car, consider downsizing to something reliable but less flashy. Trading a $450 monthly payment for a $200 payment saves $3,000 annually – money that could grow significantly when invested.

Public transportation, biking, or walking can eliminate car expenses entirely in many cities. Calculate the true cost of car ownership: payments, insurance, gas, maintenance, and parking often exceed $800 monthly. Even expensive monthly transit passes rarely cost more than $150.

For those needing cars, buy used vehicles 2-4 years old to avoid the steepest depreciation. Shop around for insurance annually – rates vary dramatically between companies. Consider pay-per-mile insurance if you drive infrequently.

Carpooling, ride-sharing for occasional trips, or car-sharing services like Zipcar can provide transportation access without full ownership costs.

Lower food costs without sacrificing nutrition

Food expenses offer tremendous savings potential through strategic planning. Meal prepping on weekends can cut your food costs in half while improving nutrition. Cooking large batches and freezing portions saves both time and money throughout the week.

Shop with a list and stick to store perimeters where fresh, whole foods live. Generic brands provide 20-40% savings over name brands for identical quality. Buy seasonal produce and freeze extras when prices drop.

Restaurant meals cost 3-5 times more than home-cooked equivalents. Limit dining out to once or twice weekly and choose lunch specials over dinner when you do. Happy hour prices and lunch portions often provide better value.

Bulk buying works for non-perishables and items you use regularly. Warehouse stores like Costco can provide significant savings if you avoid impulse purchases and focus on staples.

Eliminate subscription services you don’t actively use

Subscription services silently drain wealth through forgotten monthly charges. The average person pays for 3-5 streaming services but actively uses only 1-2. Cancel unused subscriptions immediately and rotate services based on content you actually want to watch.

Review bank and credit card statements monthly for recurring charges. Gym memberships, software subscriptions, and premium app features often continue billing long after you stop using them. Many companies make cancellation difficult – persist and document your cancellation requests.

Share subscription costs with family or friends where terms allow. Family plans for music streaming, cloud storage, and streaming services provide significant per-person savings.

Consider free alternatives before paying for premium services. Many paid apps have capable free counterparts, and library systems often provide free access to streaming services, audiobooks, and digital magazines.

Set calendar reminders before free trials end to avoid automatic charges for services you don’t want to continue.

Generate Additional Income Streams

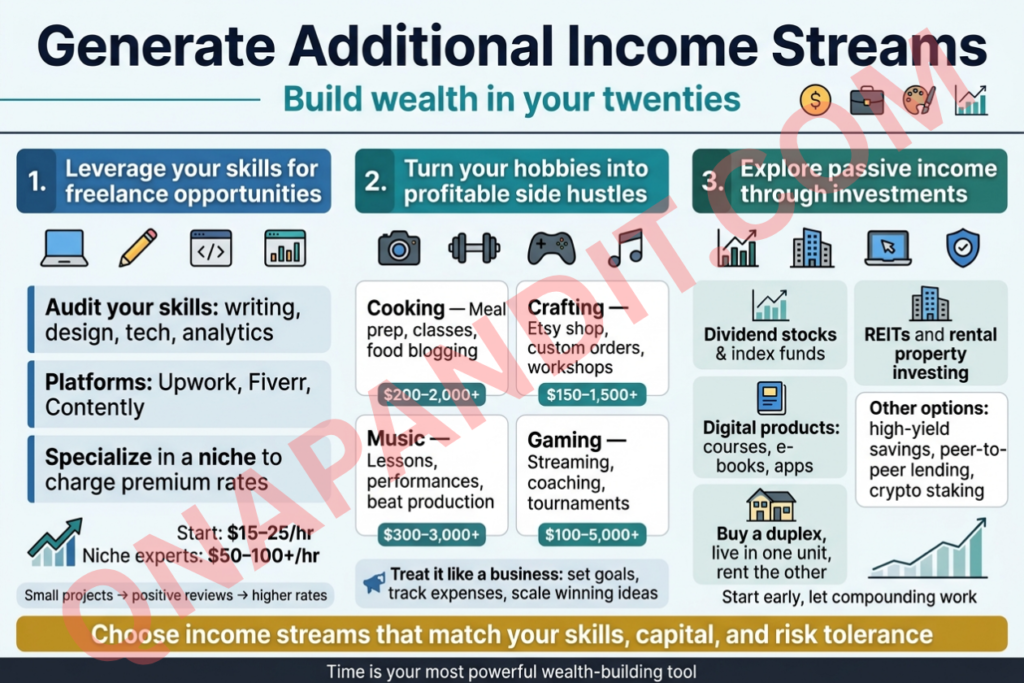

Leverage your skills for freelance opportunities

The gig economy has opened doors that simply didn’t exist for previous generations. Your existing skills—whether technical, creative, or analytical—can become immediate income sources without waiting years for traditional career advancement.

Start by auditing your current abilities. Can you write? Platforms like Upwork, Fiverr, and Contently connect writers with businesses needing content. Are you tech-savvy? Web development, graphic design, and social media management are consistently in high demand. Even seemingly basic skills like data entry or virtual assistance can generate $15-25 per hour.

The key is positioning yourself strategically. Instead of competing on price alone, focus on a specific niche where you can command premium rates. A freelance writer specializing in fintech content earns significantly more than a general copywriter. A graphic designer who understands e-commerce brands can charge 2-3x standard rates.

Build your reputation methodically. Start with smaller projects to gather positive reviews, then gradually increase your rates as your portfolio grows. Many successful freelancers earning $50-100+ per hour started exactly this way during their twenties.

Turn your hobbies into profitable side hustles

Your personal interests likely contain untapped earning potential. The beauty of monetizing hobbies lies in doing work that doesn’t feel like work while building wealth in your twenties.

Photography enthusiasts can shoot local events, portraits, or stock photos. Fitness lovers might become personal trainers or create workout programs. Gamers can stream on Twitch or create YouTube content. Even seemingly niche interests like board game design or urban gardening have thriving online communities willing to pay for expertise.

Consider these proven hobby-to-income transformations:

| Hobby | Potential Income Streams | Monthly Earnings Range |

|---|---|---|

| Cooking | Meal prep services, cooking classes, food blogging | $200-2,000+ |

| Crafting | Etsy shop, custom orders, workshop teaching | $150-1,500+ |

| Music | Lessons, event performances, beat production | $300-3,000+ |

| Gaming | Streaming, coaching, tournament participation | $100-5,000+ |

The transition from hobby to business requires treating it seriously. Set specific income goals, track expenses, and gradually scale successful ventures. Many people stumble by keeping their side hustles too casual—approach them with the same professionalism you’d bring to any business venture.

Explore passive income through investments

Passive income represents the ultimate goal for long-term wealth building. While it requires upfront effort or capital, the compounding effects over time create financial freedom that traditional employment alone rarely achieves.

Start with dividend-paying stocks and index funds. Companies like Coca-Cola, Johnson & Johnson, and Realty Income have paid consistent dividends for decades. Even small monthly investments of $100-200 can grow substantially over time through reinvestment. REITs (Real Estate Investment Trusts) offer another accessible entry point into real estate without requiring massive capital or property management responsibilities.

For those with slightly more capital, consider rental property investing. House hacking—buying a duplex, living in one unit, and renting the other—can eliminate housing costs while building equity. Many successful real estate investors started this exact way in their twenties.

Digital products create scalable passive income streams. Online courses, e-books, mobile apps, or subscription-based content can generate ongoing revenue after initial creation. The beauty of digital products lies in unlimited reproduction without additional manufacturing costs.

Peer-to-peer lending platforms, high-yield savings accounts, and even cryptocurrency staking (with proper research and risk management) offer additional passive income opportunities for young adults just starting their financial journey.

Remember that true passive income often requires active work upfront. The key is choosing investments and ventures that align with your risk tolerance, available capital, and long-term financial goals. Starting early gives you the most powerful wealth-building tool available: time.

Automate Your Savings for Guaranteed Success

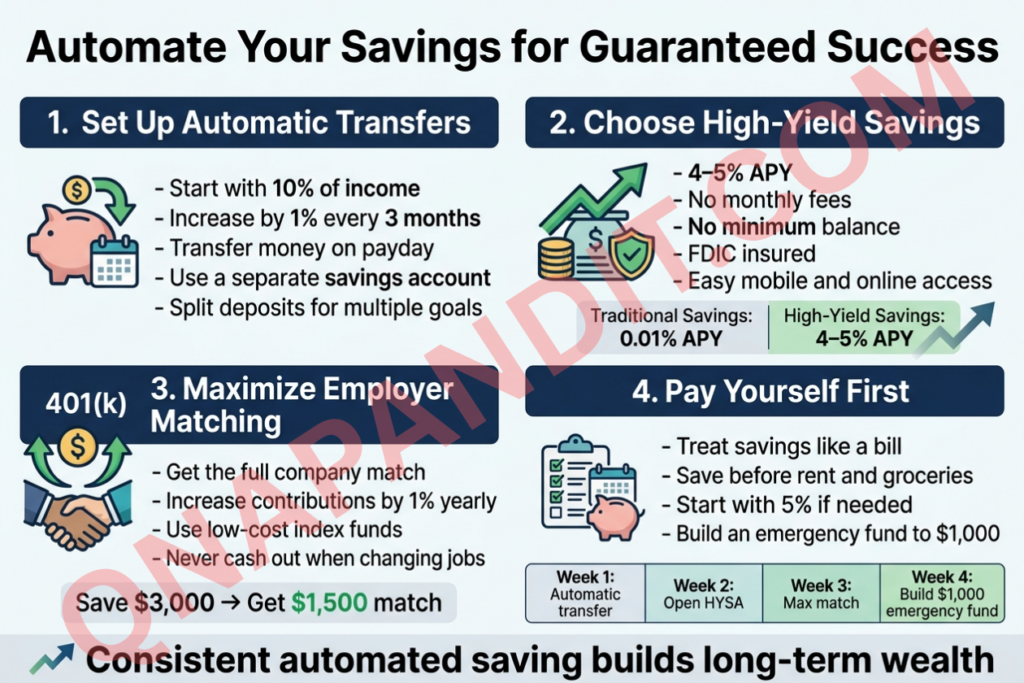

Set up automatic transfers to savings accounts

The biggest obstacle to building wealth isn’t earning more money—it’s the human tendency to spend whatever’s sitting in your checking account. Automated savings strategies eliminate this problem by moving money before you have a chance to spend it.

Start by setting up automatic transfers that happen the day after your paycheck hits your account. Most banks allow you to schedule recurring transfers between accounts, and many employers offer direct deposit splitting that sends portions of your paycheck to different accounts automatically.

Best practices for automatic transfers:

- Start with 10% of your income and increase by 1% every three months

- Transfer money on payday when your account balance is highest

- Use a separate savings account that’s not linked to your debit card

- Set up multiple automatic transfers for different goals (emergency fund, vacation, down payment)

The key is making it invisible. When the money never appears in your checking account, you quickly adapt your spending habits around what’s actually available.

Use high-yield savings accounts to maximize growth

Traditional savings accounts pay around 0.01% interest, which means your money loses value to inflation every year. High-yield savings accounts typically offer 4-5% annual percentage yield, making your automated savings strategies significantly more effective.

Top features to look for:

- No monthly fees or minimum balance requirements

- Easy online and mobile access

- FDIC insurance protection

- Competitive interest rates that adjust with market conditions

Online banks like Marcus, Ally, and Capital One consistently offer the highest rates because they don’t maintain expensive physical branches. The difference is substantial: $10,000 in a traditional savings account earns about $1 per year, while the same amount in a high-yield account generates $400-500 annually.

Take advantage of employer matching programs

Employer 401(k) matching is literally free money, yet 25% of eligible employees don’t participate. This is one of the most powerful wealth building in 20s strategies available.

Common matching formulas:

- 50% match up to 6% of salary

- 100% match up to 3% of salary

- Dollar-for-dollar match up to 4% of salary

If your employer matches 50% of contributions up to 6% of your salary, and you earn $50,000, contributing $3,000 (6%) gets you an additional $1,500 from your employer—a guaranteed 50% return on investment.

Steps to maximize employer matching:

- Contribute at least enough to get the full company match

- Increase contributions by 1% annually or whenever you get a raise

- Choose low-cost index funds within your 401(k) options

- Never cash out your 401(k) when changing jobs

Implement the pay-yourself-first strategy

Pay-yourself-first means treating savings like a non-negotiable bill that gets paid before rent, groceries, or entertainment. This mindset shift transforms personal finance for young professionals by prioritizing your future over immediate wants.

Implementation timeline:

| Week 1 | Set up automatic transfer for 10% of income |

| Week 2 | Open high-yield savings account |

| Week 3 | Maximize employer 401(k) matching |

| Week 4 | Increase emergency fund to $1,000 minimum |

The strategy works because it removes decision fatigue from saving. Instead of hoping you’ll have money left over each month, you guarantee it by paying your future self first. After three months, you won’t miss the money because your spending naturally adjusts to your new “take-home” amount.

Start small if 10% feels overwhelming—even 5% creates the habit and momentum needed for long-term wealth building in 20s. The compound effect of consistent automated saving far outweighs the impact of any single large contribution.

Conclusion

The difference between those who build wealth and those who don’t comes down to five fundamental practices: smart money management, following the 50/30/20 rule, cutting down major expenses, creating multiple income sources, and setting up automatic savings. These aren’t complicated strategies that require a finance degree – they’re simple habits that anyone can start today.

Your twenties are the perfect time to get this right because time is your biggest advantage. Every dollar you save and invest now has decades to grow. Start with automating just $50 a month into savings, track where your money goes for one week, or pick up one side hustle that interests you. Small steps now will put you miles ahead of your peers who are still wondering where their paycheck went.