How much of my income should I save each month?

Latest News & Updates

QNAPANDIT Latest Articles

How to Start Crypto Staking in India: Earn Passive Crypto Income

Crypto staking lets you earn passive income from your digital assets while supporting blockchain networks. If you’re an Indian crypto investor looking to generate steady returns without active trading, staking offers a compelling opportunity to put your cryptocurrency to work. This guide is designed for beginners who want to start earning crypto staking rewards in […]

Email Marketing for Small Business 2026: Grow Your List

Small business owners face endless marketing challenges in 2026, but email marketing offers a clear solution that cuts through the noise. While social algorithms change overnight and ad costs keep rising, your email list remains yours—a direct connection to customers that no platform can take away. This guide is for small business owners, entrepreneurs, and […]

The Ultimate Guide to Crafting AI Prompts That Work

Good AI prompts can make or break your results, but most people waste time on prompting “hacks” that don’t actually work. This guide is for anyone using AI tools like ChatGPT, Claude, or other language models who wants to get better outputs without falling for the latest prompt influencer trends. You’ll learn practical techniques that […]

10 Online Business Ideas Under ₹50,000 (India, 2026 Edition)

Starting an online business in India doesn’t need to break your bank account. With just ₹50,000, you can launch a profitable venture from your home and tap into India’s booming digital economy. This guide is perfect for college students, working professionals seeking side income, and aspiring entrepreneurs who want to start small and scale smartly. […]

Fixed vs. Growth Mindset: Which One Wins?

Your mindset shapes everything—from how you handle setbacks to whether you even try new things. This deep dive is for entrepreneurs, business leaders, and anyone curious about growth mindset vs fixed mindset psychology who wants to understand which approach actually drives success. Many people believe talent and intelligence are set in stone. But research shows […]

Transforming the Educational Landscape: The Value of an Education Franchise in Nigeria

The global demand for high-quality supplementary learning has witnessed a dramatic surge over recent years. In rapidly developing economies, traditional academic structures face massive challenges trying to keep pace with the cognitive and technological skills required for the modern global workforce. As a result, parents are increasingly looking for specialized programs that go beyond basic […]

How to Write a Business Plan (India, 2026): Step-by-Step

Starting a business in India has never been more accessible, but turning your idea into reality still requires a solid plan. This comprehensive guide shows you how to write a business plan that actually works for Indian entrepreneurs in 2026. This step-by-step business plan guide is designed for first-time entrepreneurs, startup founders, and small business […]

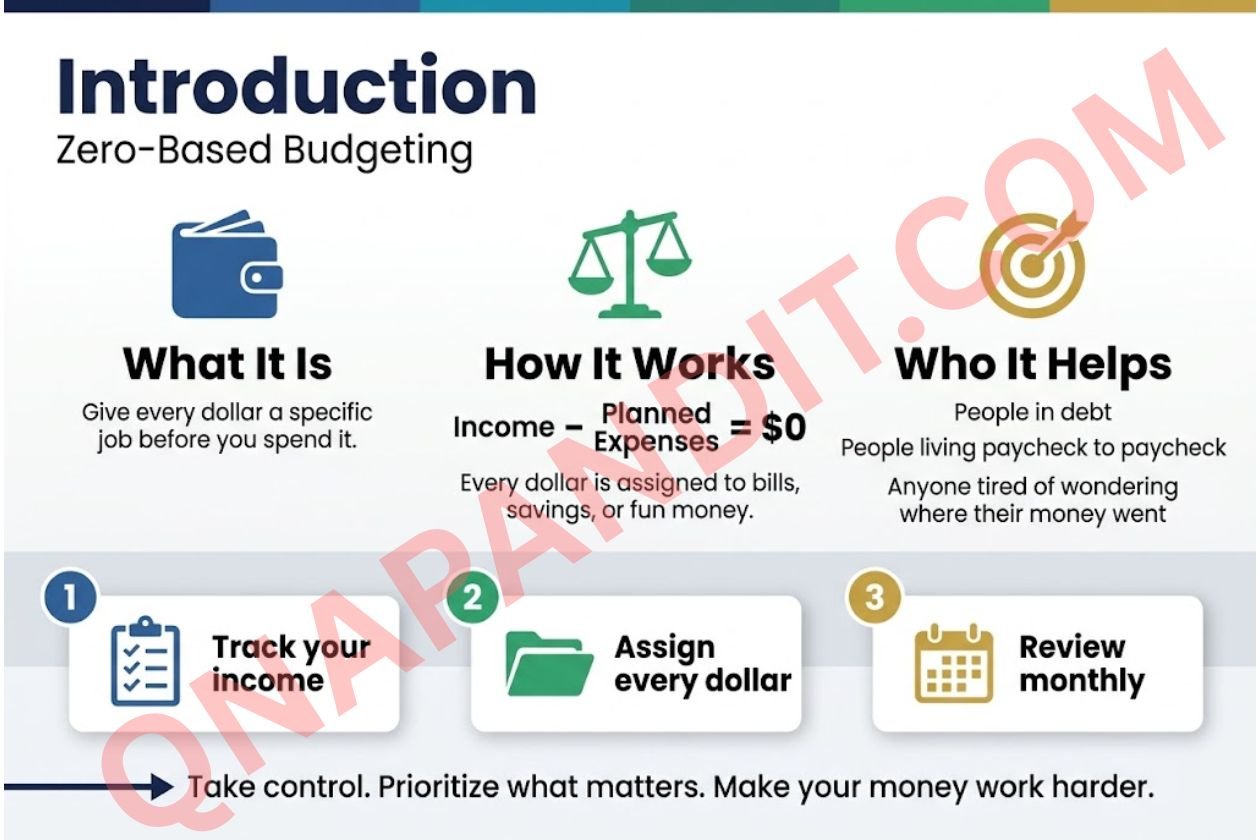

2026 Budget Planner for Beginners: Zero-Based Budgeting Guide

Ready to take control of your money in 2026? Zero-based budgeting might be exactly what you need to finally see where every dollar goes. This 2026 budget planner for beginners will show you how zero-based budgeting works – a simple method where your income minus expenses equals zero every month. Don’t worry, that doesn’t mean […]

The Ultimate SEO Toolkit: 5 Must-Have Tools for 2026

SEO success in 2026 demands more than traditional keyword stuffing and link building. You need tools that can navigate AI-powered search engines, track your brand’s visibility in ChatGPT responses, and optimise for Google’s AI Overviews alongside classic organic rankings. This guide is designed for digital marketers, content creators, SEO professionals, and business owners who want […]

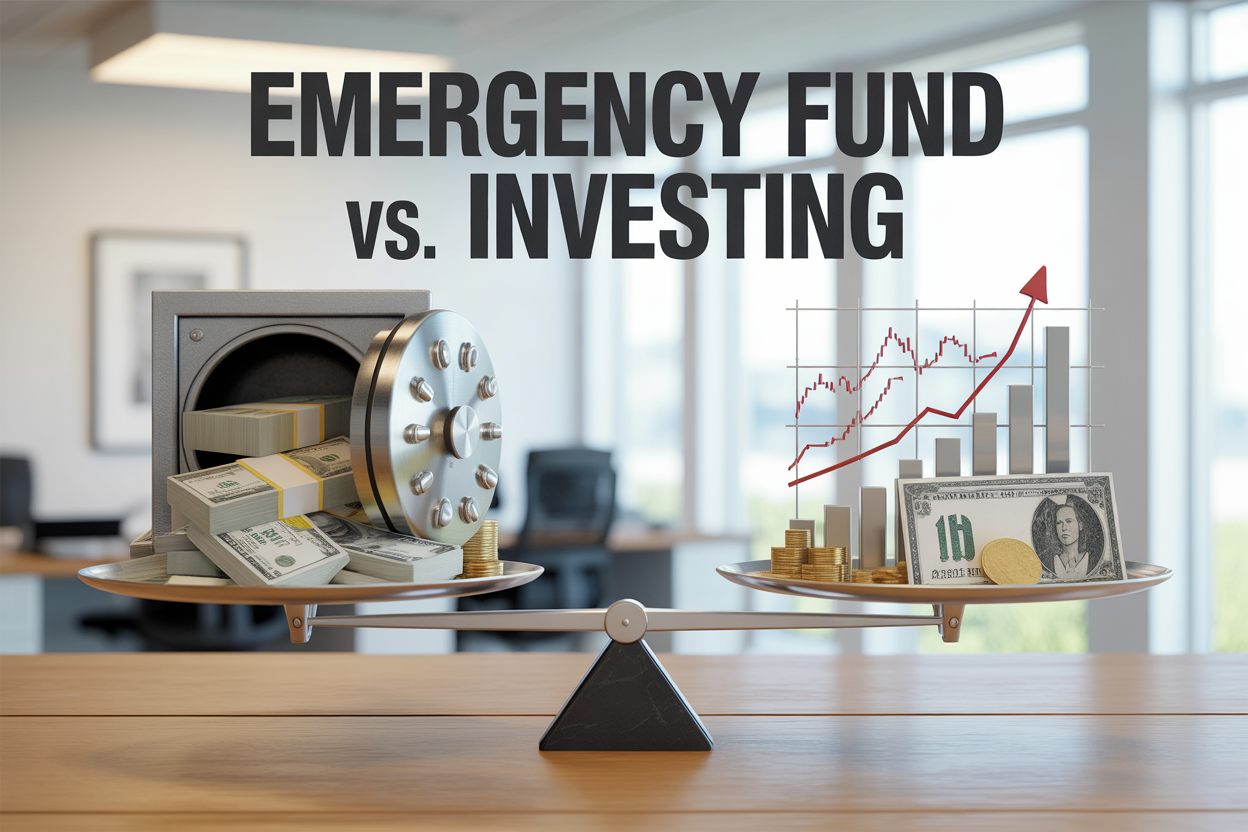

Emergency Fund vs. Investing: Which Should Come First?

You’ve got money to manage, but you’re stuck on a big question: Should you build an emergency fund or start investing first? This decision stumps many people, especially young adults and new earners who want to grow wealth but also need financial security. You know investing can make your money grow over time, but emergencies […]

Why Closing Old Credit Cards Could Destroy Your Score

Closing old credit cards can tank your credit score in ways most people don’t expect. This guide is for anyone considering cancelling old cards, whether you’re decluttering your wallet or avoiding annual fees. Your credit score takes a hit primarily because closing credit cards affects your credit utilisation ratio. When you lose that available credit […]

Crypto Portfolio Strategy 2026: Safe Diversification in INR

Building a smart crypto portfolio in 2026 means more than just buying Bitcoin and hoping for the best. With institutional money pouring into crypto ETFs and new asset classes like tokenised real estate hitting the scene, Indian investors need a structured approach to spread risk across this volatile market while keeping their rupee investments safe. […]

Why PAA Questions Are SEO Gold (And How to Mine Them)

Google’s People Also Ask boxes appear in over 43% of search results, yet most marketers ignore this goldmine of SEO opportunities. PAA questions reveal exactly what your audience wants to know, giving you a direct path to featured snippets, voice search optimization, and higher rankings. This guide is for content marketers, SEO specialists, and business […]

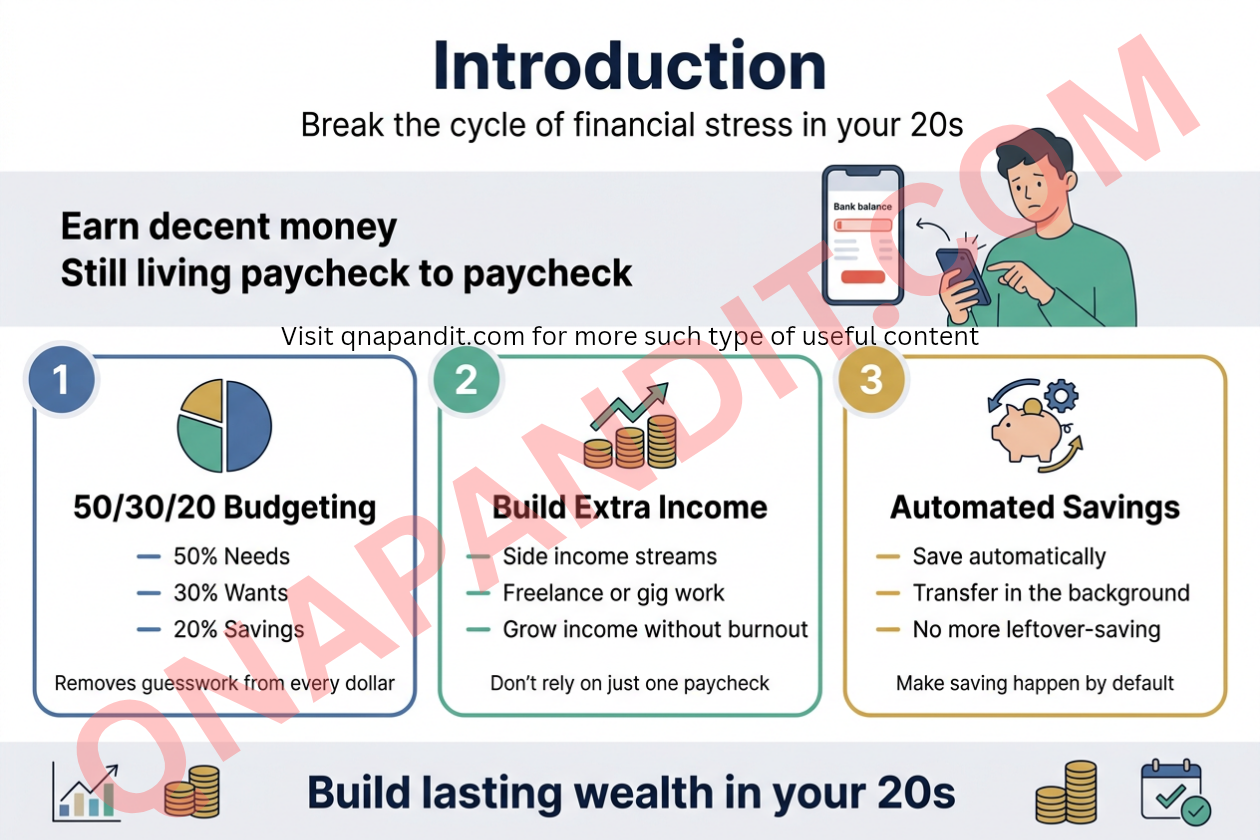

Why 99% of People in Their 20s Never Build Wealth (And How to Be the 1%)

Most twenty-somethings earn decent money but still live paycheck to paycheck. They watch their bank account hover near zero while wondering why wealth building in their 20s feels impossible for them, but easy for others. This guide is for young adults who want to break the cycle of financial stress and join the small group […]

How to Turn Your Hobby Into a Profitable Career Skill

Your hobby feels more like an escape from work than just a weekend activity. We get it—that creative spark or hands-on satisfaction you find in photography, cooking, woodworking, or whatever gets you excited might actually be pointing toward your next career move. This guide is for anyone tired of watching the clock at their day […]

99% of Indians Don’t Know These 7 Passive Income Secrets That Actually Work in 2026

Most Indians work hard but stay financially stressed because they rely on just one income source. The traditional advice of “save more, spend less” only gets you so far when your salary barely keeps up with rising costs. The passive income secrets that actually work in 2026 aren’t the typical “make money while you sleep” […]

Local SEO for Indian SMBs: Step-by-Step Optimisation

Getting found online shouldn’t feel impossible for small business owners in India. When someone searches “dentist near me” or “best restaurant in Koramangala,” your business deserves to show up first – not buried on page two where nobody looks. Local SEO for Indian SMBs is your roadmap to dominating search results in your area. This […]

Understanding Your Audience: The Foundation of Resonance

Why Audience Understanding is Non-Negotiable Creating content without understanding your audience is like shooting arrows in the dark – you might occasionally hit something, but most efforts miss their mark entirely. Audience understanding forms the bedrock of effective content strategy, transforming generic information into powerful messaging that resonates. When you deeply understand your audience, you […]

Trump’s India Tariff Threat: What It Means for Oil Markets

President Trump’s latest threat to impose additional tariffs on India for continuing to import Russian oil has sent ripples through global energy markets. This move targets India’s strategic decision to maintain energy security through discounted Russian crude purchases, despite existing U.S. sanctions and trade pressures. For energy traders, policy analysts, and oil market investors, understanding […]

Zero-Based Budgeting Explained: How to Budget Every Dollar (Step-by-Step Guide)

Zero-based budgeting is a simple money management strategy where you give every dollar of your income a specific job before you spend it. This method works great for anyone who wants to take complete control of their finances—whether you’re drowning in debt, barely making ends meet, or just tired of wondering where your paycheck went […]

Building Your First Team: Hiring for Your Small Business

Hiring your first employee marks a major milestone for any small business owner. You’re moving from a one-person operation to building a real team—and that’s both exciting and scary. This guide is for small business owners and entrepreneurs ready to make their first hires or expand their existing teams. We’ll walk you through everything from […]

The Shocking Truth About Home Yoga That Studios Don’t Want You to Know

Studios charge premium prices for what we can achieve right in our living rooms – and the home yoga benefits often surpass traditional classes. This guide is for busy people who want to start yoga at home, for beginners, experienced practitioners seeking flexibility, and anyone tired of expensive studio memberships that don’t fit their schedule. […]

The Ultimate Guide to Understanding Monthly Credit Score Swings

Your credit score doesn’t stay the same from month to month, and those monthly credit score changes can feel confusing and stressful. This comprehensive guide breaks down everything you need to know about credit score fluctuations and helps you take control of your financial health. Who this guide is for: Anyone who’s noticed their credit […]

5 Crypto Investing Mistakes and How to Avoid Them

Cryptocurrency investing in India is growing rapidly, but many new investors make costly mistakes that could have been avoided with better preparation. This guide is designed for beginners and intermediate investors who want to build a profitable crypto portfolio while staying safe and compliant with Indian regulations. New crypto investors often lose money because they […]

Social Media Marketing on a Budget: Small Biz Strategies

Small business owners know they need a strong social media presence, but many worry about the costs. The truth is, you don’t need a massive marketing budget to succeed on social platforms. Smart small business social media strategies can deliver real results without breaking the bank. This guide is for small business owners, entrepreneurs, and […]

The Ultimate Guide to Boosting Your Credit Score in 90 Days

A poor credit score can cost you thousands of dollars in higher interest rates and limit your access to loans, apartments, and even some jobs. If you’re dealing with bad credit from past mistakes, preparing for a major purchase, or simply want to improve your financial standing, this 90-day credit improvement plan can help you […]

The Ultimate Guide to Cybersecurity for Small Businesses

Small business owners face a growing number of cyber threats that can devastate operations, finances, and reputation. This comprehensive guide is designed for entrepreneurs, small business owners, and team leaders who need practical cybersecurity solutions without breaking the bank or requiring technical expertise. Cybercriminals increasingly target small businesses because they often lack robust security measures. […]

Timur Turlov and the Global Development of Freedom Holding

In recent years, financial entrepreneur Timur Turlov has attracted attention in the global finance sector as the founder and CEO of Freedom Holding Corp. As financial markets become more interconnected and technology reshapes how investors access global exchanges, companies like Freedom Holding represent a broader shift toward modern, digital-driven financial services. Freedom Holding Corp. operates […]

When it comes to saving a portion of your income each month, it's essential to strike a balance between meeting your current financial needs and securing your future financial stability. While the exact percentage may vary based on individual circumstances, financial experts generally recommend follRead more

When it comes to saving a portion of your income each month, it’s essential to strike a balance between meeting your current financial needs and securing your future financial stability. While the exact percentage may vary based on individual circumstances, financial experts generally recommend following the 50/30/20 rule for personal finance:

– 50% for Needs: Allocate approximately 50% of your income towards essential expenses like housing, utilities, groceries, transportation, and insurance.

– 30% for Wants: Reserve around 30% for discretionary spending on non-essential items such as dining out, entertainment, hobbies, and shopping.

– 20% for Savings: Aim to save at least 20% of your income each month. This portion can go towards various savings goals, including emergency fund, retirement savings, investments, and other financial objectives.

By prioritizing savings and making it a non-negotiable part of your budget, you establish a healthy financial habit that can lead to long-term wealth accumulation and financial security.

Remember, the key to successful saving is consistency and discipline. Automating your savings through direct deposit or setting up recurring transfers to a separate savings account can help you stay on track without the temptation to spend the money elsewhere.

Additionally, consider optimizing your savings by:

– Regularly reviewing and adjusting your budget to ensure your savings rate aligns with your financial goals.

– Maximizing contributions to tax-advantaged accounts like 401(k)s, IRAs, or other retirement savings

See less