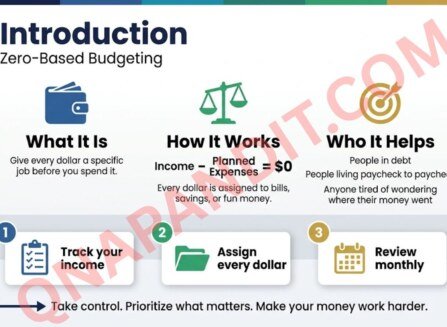

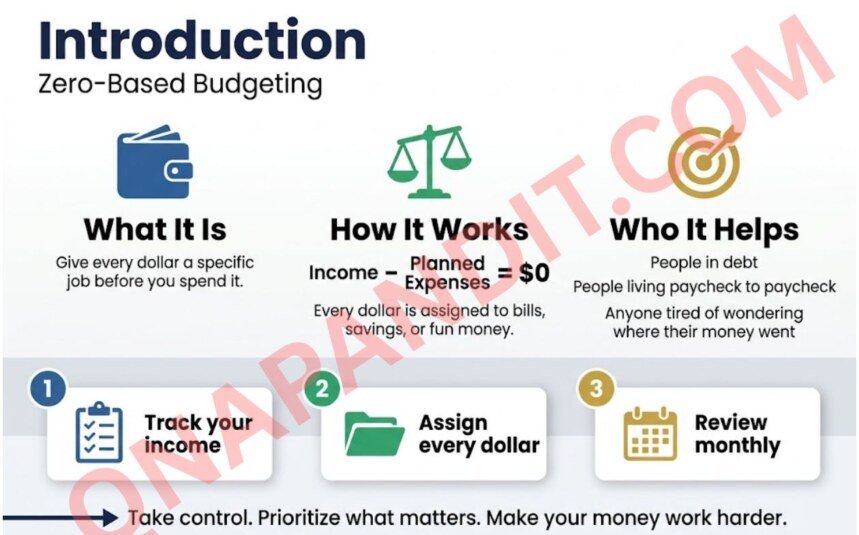

Zero-based budgeting is a simple money management strategy where you give every dollar of your income a specific job before you spend it. This method works great for anyone who wants to take complete control of their finances—whether you’re drowning in debt, barely making ends meet, or just tired of wondering where your paycheck went every month.

Unlike other budgeting approaches that use fixed percentages or complicated rules, zero-based budgeting adapts to your real life each month. Your income minus all your planned expenses should equal zero, meaning every single dollar gets assigned to something important: paying bills, saving for goals, or even fun money.

In this guide, you’ll learn the step-by-step zero-based budget creation process that takes just five simple steps to master. We’ll also cover smart expense allocation strategies that help you prioritise what matters most, and show you practical monthly budget tracking techniques that keep you on track all month long. By the end, you’ll have everything you need to stop your money from disappearing and start making it work harder for your goals.

Understanding Zero-Based Budgeting Fundamentals

What Zero-Based Budgeting Really Means

Zero-based budgeting is a comprehensive financial framework that assigns a specific purpose to every dollar of your take-home pay. The core principle revolves around ensuring that your income minus all planned expenses and savings equals exactly zero each month. This doesn’t mean spending every penny you earn – rather, it means being intentional about where every dollar goes.

In zero-based budgeting, nothing happens to your money by chance. As financial experts note, “A zero-based budget is very intentional. There is no unplanned free cash or spending.” This approach requires you to actively decide how to allocate each dollar before the month begins, including portions designated for savings goals, emergency funds, and retirement planning.

The method gets its name because you start from a “zero base” each budgeting period. Unlike traditional budgeting approaches that build upon previous budgets with incremental increases, zero-based budgeting requires justifying every expense from scratch. You must analyse and justify each cost, focusing on your current financial objectives and priorities.

This budgeting style provides greater insight into your finances while offering the flexibility to customise your budget month to month. You set the rules and can adapt your plan as your income, needs, and wants change, making it a highly personalised approach to financial management.

How Zero-Based Budgeting Differs from Living Paycheck to Paycheck

The distinction between zero-based budgeting and living paycheck to paycheck lies in intentionality and planning. While both scenarios might result in spending most or all of your monthly income, the approach and outcomes are fundamentally different.

Living paycheck to paycheck typically involves spending money throughout the month without a predetermined plan, hoping something remains for savings. This reactive approach often leads to financial stress and limited progress toward financial goals. People in this situation usually “spend first throughout the month and only save whatever is left over, assuming there is anything left at all.”

Zero-based budgeting flips this approach entirely. It operates on the principle of paying yourself first by deciding at the beginning of the month how much you want to save before allocating money to expenses. This proactive planning ensures that savings goals are prioritised rather than treated as an afterthought.

With zero-based budgeting, you maintain complete control over your financial decisions. You’ll decide in advance how many meals you’ll eat out, what entertainment you’ll purchase, and which discretionary expenses you’ll allow. This planning helps curb impulse spending and prevents overextending yourself financially.

The method also provides a clearer view of your financial means, forcing you to identify which discretionary costs you actually value and which you can eliminate. This might reveal passive payments for unused subscriptions or services that no longer serve your goals.

Common Misconceptions About Spending All Your Money

One of the most persistent misconceptions about zero-based budgeting is that it encourages reckless spending or requires you to spend every dollar you earn. This fundamental misunderstanding stems from the “zero” terminology, which some interpret as leaving no money unallocated rather than ensuring every dollar has a purpose.

The reality is that zero-based budgeting strongly emphasises savings and financial security. A properly constructed zero-based budget allocates significant portions of income to various savings categories, including emergency funds, retirement contributions, and specific financial goals. The “zero” refers to the mathematical equation where income minus all planned expenses and savings equals zero, not to your remaining bank balance.

Another common misconception suggests that zero-based budgeting prevents you from having any financial flexibility or emergency funds. In practice, the opposite is true. By deliberately planning for savings and emergency expenses within your budget, you create greater financial stability and flexibility. The method actually encourages building robust emergency savings as part of your regular budget allocation.

Some people also believe that zero-based budgeting is too restrictive compared to other budgeting methods. While it does require more upfront planning and ongoing attention, it offers greater customisation than rigid percentage-based systems. Unlike strategies that assign fixed percentages to spending categories, zero-based budgeting allows you to adjust allocations based on your changing circumstances and priorities.

The intensive planning requirement is sometimes viewed as a disadvantage, but this detailed approach ensures that every financial decision aligns with your current goals and values, ultimately leading to better financial outcomes and reduced money-related stress.

Essential Preparation Steps Before Creating Your Budget

Calculate Your Total Monthly Income Including Side Hustles

Before creating your zero-based budget, you need an accurate picture of all the money flowing into your household. Start by identifying every source of income you receive throughout the month. This comprehensive approach ensures you’re accounting for every dollar that comes your way.

Your primary income sources include your salary or wages from your main job. However, don’t stop there – include all additional revenue streams such as side hustles, freelance work, part-time jobs, or gig economy earnings. Investment income from dividends, interest, or rental properties should also be factored in, along with any other sources like child support, alimony, or government benefits.

Tips for accurate income calculation:

- Always use your net income (take-home pay after taxes and deductions) rather than gross income to understand your actual available funds

- If you have irregular or fluctuating income, consider averaging your earnings over several months for a more realistic estimate.

- For contractors or self-employed individuals, remember to set aside a percentage for taxes since your income may be gross pay without taxes deducted.

Track Your Current Spending Patterns for Several Months

Understanding where your money currently goes is vital for effective zero-based budgeting. Begin by tracking all your expenses for at least several months to identify patterns and habits in your spending behaviour.

Use expense tracking methods that work for your lifestyle – whether that’s budgeting apps, spreadsheets, or traditional pen and paper. Review your bank statements thoroughly to identify recurring expenses and spending patterns you might have overlooked.

Essential tracking practices:

- Record every expense, no matter how small, to gain a complete understanding of your financial habits

- Keep receipts if you use cash frequently

- For credit and debit purchases, examine your statements carefully

- Include one-off purchases and recurring charges like streaming services and fitness apps

- Don’t forget peer-to-peer payment networks (Apple Cash, Zelle, Venmo, CashApp, or Google Pay)

Being honest about your spending is crucial – this data will form the foundation of your zero-based budget and help you make informed decisions about where every dollar should go.

Categorise All Your Expenses and Financial Priorities

Once you’ve tracked your spending patterns, organise all expenses into clear categories. This step is essential for zero-based budgeting since you’ll need to allocate every dollar to specific categories.

Start by separating your expenses into two main groups:

Fixed Expenses remain constant each month and include:

- Rent or mortgage payments

- Insurance premiums

- Loan payments

- Utilities

Variable Expenses fluctuate monthly and can be adjusted, such as:

- Groceries

- Dining out

- Entertainment

- Clothing

- Transportation costs

Beyond basic expense categories, establish your financial priorities by setting both short-term and long-term goals. Short-term goals might include building an emergency fund, saving for a vacation, or paying off a credit card within the year. Long-term goals could encompass saving for a home, retirement planning, or education savings for children.

When setting these financial priorities, make them specific and measurable rather than vague. For example, instead of “save money,” specify “save $5,000 for vacation by next summer.” Ensure your goals are realistic based on your income and expenses – while it’s great to be ambitious, unattainable goals can lead to frustration and budget abandonment.

Step-by-Step Zero-Based Budget Creation Process

List All Sources of Monthly Income

Now that we understand the fundamentals of zero-based budgeting, let’s dive into the step-by-step zero-based budget creation process. The foundation of any effective zero-based budget begins with identifying exactly how much money you have coming in each month.

Start by calculating your total monthly take-home pay from your primary job. Check your pay stubs or bank account direct deposits to determine your after-tax income. This is the actual amount you receive each month, not your gross salary before deductions.

Don’t forget to include all additional income sources:

- Side hustle or gig work earnings

- Freelance income

- Rental property income

- Investment dividends

- Any other regular money flowing into your accounts

For Variable Income Earners:

If your income fluctuates month to month, review the past year’s earnings and identify your lowest-grossing months. Use these conservative figures as your baseline for budgeting to ensure you don’t overspend. When you earn more in higher-income months, you can allocate the extra funds to savings, debt repayment, or discretionary expenses.

Plan Your Expenses in Priority Order

With your income clearly defined, the next crucial step in the zero-based budget creation process is systematically planning your expenses. Review your previous months’ credit card and bank statements to understand where your money typically goes.

Organise expenses by priority:

Essential Expenses (Highest Priority):

- Housing costs (rent/mortgage, utilities)

- Groceries and basic food needs

- Transportation expenses

- Minimum debt payments

- Insurance premiums

- Medical costs

Important but Flexible:

- Emergency fund contributions

- Retirement savings

- Other savings goals

Discretionary Spending (Lowest Priority):

- Entertainment and dining out

- Shopping and personal care

- Travel and hobbies

- Subscription services

Break your needs and wants into specific subcategories for better tracking. Set target amounts for each category based on your historical spending patterns and current financial goals.

Assign Every Dollar Until Income Minus Expenses Equals Zero

This is where zero-based budgeting gets its name – you’re aiming for your income minus all planned expenses and savings to equal exactly zero. Every dollar must have a designated purpose before the month begins.

The Assignment Process:

- Start with your total monthly income

- Allocate money to essential expenses first

- Assign funds to savings goals (emergency fund, retirement)

- Distribute remaining dollars to discretionary categories

- Continue until every dollar has a job

Remember, reaching zero doesn’t mean spending everything you earn. A significant portion should be allocated to various savings goals. As financial expert Beau Zhao notes, “A zero-based budget is very intentional. There is no unplanned free cash or spending.” This approach essentially means paying yourself first by proactively planning your savings at the start of each month.

Handle Budget Adjustments When Numbers Don’t Balance

When creating your zero-based budget, you’ll likely encounter situations where your initial calculations don’t balance perfectly. Here’s how to handle common scenarios:

If You Have a Negative Number (Spending More Than Income):

This indicates you’re planning to spend beyond your means. Review your nonessential expenses and decide what can be reduced or eliminated. Focus on discretionary categories like entertainment, dining out, and subscription services.

You may need to make tough choices, but consistently overspending will derail your financial health by forcing you to drain savings or accumulate debt.

If You Have a Positive Number (Leftover Money):

Congratulations – you have extra money to allocate! First, ensure you’re adequately funding emergency savings and retirement goals. If those are on track, you can assign the remaining funds to additional savings goals, debt repayment, or discretionary spending categories you value most.

Making Mid-Month Adjustments:

Real life rarely follows your exact budget plan. When unexpected expenses arise or you overspend in one category, you’ll need to reallocate money from other categories to maintain your zero-based balance. This flexibility is part of what makes zero-based budgeting so effective – it forces you to make conscious decisions about every financial choice throughout the month.

Smart Expense Allocation Strategy

Start with Giving and Generosity Goals

When implementing your zero-based budget allocation strategy, the first dollars should be directed toward giving and generosity goals. This foundational step ensures that charitable contributions and generosity remain a priority before other expenses consume your available income.

By allocating funds to giving first, you maintain alignment with your values and establish a practice of intentional generosity that might otherwise be overlooked when money gets tight.

Consider setting a specific percentage or dollar amount for charitable giving, community support, or helping family members. This approach transforms generosity from an afterthought into a strategic financial decision that receives proper justification, much like every other expense in your zero-based budgeting process.

Prioritise Savings and Debt Payments

After establishing your giving goals, the next critical allocation involves savings and debt payments. This priority ensures your financial future remains secure while addressing existing obligations. Your emergency fund should receive attention first, as it provides the financial cushion necessary to maintain your granular budget plan during unexpected circumstances.

Following emergency savings, focus on debt repayment strategies that align with your overall financial objectives. Whether targeting high-interest debt first or following a debt snowball approach, these payments require justification just like any other expense in your budget. Additionally, allocate funds toward retirement savings, investment goals, and other long-term financial objectives.

This strategic approach to savings and debt payments prevents these crucial elements from being treated as optional expenses that only receive leftover funds.

Cover the Four Walls: Food, Utilities, Housing, Transportation

With giving and savings addressed, turn your attention to covering the four essential expense categories that form the foundation of your daily life: food, utilities, housing, and transportation. These represent your non-negotiable expenses that require funding before any discretionary spending occurs.

Housing costs, including rent or mortgage payments, property taxes, and insurance, typically represent your largest expense category and must be thoroughly justified within your zero-based budget. Transportation expenses encompass vehicle payments, fuel, maintenance, insurance, and public transportation costs necessary for work and essential activities.

Utility expenses include electricity, gas, water, internet, and phone services required for basic living. Food allocation covers groceries and essential meal planning, ensuring adequate nutrition while maintaining cost efficiency. Each of these categories requires careful analysis to ensure every dollar serves a specific purpose in maintaining your household operations.

Allocate Remaining Funds to Other Expenses and Fun Money

Once your essential four walls are covered, the remaining funds in your zero-based budget can be allocated to other necessary expenses and discretionary spending. This final allocation step ensures that every remaining dollar receives proper justification and serves a specific purpose in your financial plan.

Other necessary expenses might include clothing, medical costs, personal care items, subscriptions, and professional development. Each expense should be evaluated for its contribution to your overall financial objectives and lifestyle goals.

Fun money allocation represents discretionary spending for entertainment, dining out, hobbies, and recreational activities. While these expenses are less critical than the four walls, they still require justification within your budget framework. Setting specific amounts for entertainment ensures you can enjoy life while maintaining financial discipline.

This comprehensive allocation strategy ensures that every dollar in your budget serves a purpose, whether addressing immediate needs, building long-term security, or enhancing your quality of life. The systematic approach prevents money from being spent without intention and maintains the core principle that your income minus expenses equals zero.

Monthly Budget Tracking and Management

Track Every Single Transaction Throughout the Month

Now that we have covered the initial budget creation process, successful zero-based budgeting requires diligent tracking of every financial transaction throughout the month. This means monitoring each purchase, payment, and expense to ensure you stay within your predetermined category allocations.

To hold yourself accountable with monthly budget tracking, you’ll need to closely and consistently monitor your spending. Every time you make a purchase, you must verify that it falls within the guidelines you established at the beginning of the month. This detailed approach prevents you from spending money you don’t have and maintains the integrity of your zero-based budget.

Consider reviewing your credit card and bank statements regularly to track where your money is actually going. Some budgeters find it helpful to check their spending daily or weekly, rather than waiting until month-end. This proactive approach allows you to catch overspending early and make necessary adjustments before your budget gets completely derailed.

The cash envelope system can be particularly effective for tracking discretionary spending categories. Take out cash for specific budget categories and portion it into labelled envelopes. Once you’ve spent all the cash for a certain category, you’re forced to stop spending in that area, providing a natural spending limit.

Adjust Categories When Overspending Occurs

Previously, I’ve mentioned that real life might have different plans than your carefully crafted budget. When overspending occurs in specific categories, you’ll need to make strategic adjustments to maintain your zero-based budget balance.

If you exceed your allocation in one category, you have several options to rebalance your budget. You can move money from another category where you’re under budget, reduce spending in other areas for the remainder of the month, or reallocate funds from your discretionary spending categories to cover the overage.

The key is addressing overspending immediately rather than letting it compound. Ask yourself whether the overspending resulted from poor planning, unexpected circumstances, or impulse purchases. If it’s due to unrealistic initial allocations, you may need to adjust your category amounts for future months based on this learning experience.

For variable expenses that you didn’t adequately account for, such as holiday purchases, wedding travel, or emergency phone replacements, consider creating a separate savings fund specifically for these irregular costs. This buffer fund, distinct from your emergency fund, can help accommodate unexpected expenses without disrupting your main budget categories.

Create a Fresh Budget Each Month Before It Begins

With this in mind, zero-based budgeting requires you to revisit and revise your financial plans monthly. Unlike other budgeting methods that use the same allocations repeatedly, this approach demands creating a completely fresh budget each month before it begins.

As you prepare your next month’s budget, compare your actual spending from the current month with your plans for the upcoming period. This review process helps you identify patterns, adjust unrealistic allocations, and account for upcoming irregular expenses or income changes.

Your monthly income, needs, and wants may fluctuate, making it essential to customise your budget accordingly. Perhaps you have a wedding to attend next month, a quarterly insurance payment due, or expect a bonus. These variables require adjusting your category allocations to accommodate changing circumstances while maintaining your zero-based approach.

If you come in under budget in certain categories at month-end, you can add the remaining amount to next month’s budget for that same category, move it to another category such as your emergency fund, or allocate it toward additional savings goals. The flexibility to redistribute unused funds is one of the key advantages of monthly budget tracking in zero-based budgeting.

This monthly reset ensures your budget remains relevant and achievable, preventing the frustration that comes from using outdated spending plans that no longer reflect your current financial reality.

Handling Special Budgeting Situations

Managing Zero-Based Budgets with Irregular Income

When your income fluctuates from month to month, traditional budgeting approaches often fall short. Zero-based budgeting with irregular income requires a foundation-first approach that prioritises stability over exact monthly predictions.

The most effective strategy is to budget based on your baseline income – the lowest consistent monthly amount you can reasonably expect. Review your past 6-12 months of income data and identify your lowest-earning months. Use this conservative figure as your default monthly budget foundation, ensuring your essential expenses fit within this amount.

Create a two-account system to smooth out income variations:

- Income Holding Account: All irregular payments flow here first

- Spending Account: Transfer a fixed “salary” monthly based on your baseline amount

This artificial salary system transforms unpredictable income into a predictable monthly cash flow for budgeting purposes.

Implement priority-based allocation within your zero-based budget. Fund categories in strict order of importance:

- Housing costs

- Food and groceries

- Utilities and insurance

- Transportation

- Minimum debt payments

- Tax savings (for self-employed individuals)

- Emergency buffer

- Discretionary spending

With this prioritised approach, even if a month comes in lower than expected, your most critical needs remain covered while optional categories can be adjusted.

Planning for Variable and Seasonal Expenses

Zero-based budgeting excels at handling predictable irregular expenses through strategic envelope allocation and sinking funds. Rather than scrambling when annual insurance premiums or holiday expenses arrive, build these costs into your monthly budget framework.

Calculate annual variable expenses by totalling predictable irregular costs such as:

- Insurance premiums (auto, home, health)

- Property taxes

- Holiday and gift spending

- Seasonal clothing needs

- Vehicle maintenance and registration

- Vacation fund contributions

Divide each annual amount by 12 to determine monthly sinking fund contributions. For example, if you spend $1,200 annually on holiday gifts, allocate $100 monthly to a dedicated holiday envelope within your zero-based budget.

Seasonal income variations require adjusted baseline calculations. If you earn significantly more during certain months (like tax preparers during tax season), calculate a conservative average that accounts for lean periods. Save excess earnings from high-income months to sustain your baseline budget during slower periods.

Use percentage-based allocation for truly variable expenses like utilities that fluctuate with the weather. Assign a realistic percentage of your baseline income to these categories, adjusting monthly as needed while maintaining your zero-based framework.

Building Buffer Funds for Unexpected Costs

Buffer funds serve as the safety net that makes zero-based budgeting resilient against life’s unpredictable expenses. Unlike traditional emergency funds that sit untouched, buffer funds actively support your monthly budgeting process.

Start with a one-month buffer in your income holding account. This initial buffer allows you to maintain consistent monthly transfers to your spending account even when income dips below your baseline. Gradually build this to cover 3-6 months of baseline expenses.

Create category-specific buffers within your zero-based budget for common unexpected expenses:

- Home repairs and maintenance

- Medical copays and deductibles

- Vehicle repairs

- Pet emergencies

- Technology replacements

Direct high-income month surpluses strategically. When monthly income exceeds your baseline, allocate extra funds using a predetermined percentage system:

- 40% to the emergency buffer

- 30% to debt payoff or investment goals

- 20% to tax savings (if self-employed)

- 10% to discretionary spending or wish list items

This systematic approach prevents lifestyle inflation while strengthening your financial foundation.

Track buffer fund usage as part of your monthly zero-based budget review. When you tap into buffer funds, prioritise replenishing them before increasing discretionary spending categories. This maintains the protective capacity that irregular income earners need most.

Zero-Based Budgeting vs Other Popular Methods

How It Compares to Traditional Budgeting

Zero-based budgeting fundamentally differs from traditional budgeting in its starting approach. While traditional budgeting takes the current period’s budget or actual performance as a base and adds incremental amounts for the new budget period, zero-based budgeting starts from a base of zero with no reference to prior periods.

Traditional budgeting operates on the premise that last month’s budget serves as a good starting point for this month. For example, if you spent $500 on groceries last month, a traditional budget would likely start with that figure as the baseline, making adjustments only for anticipated changes like inflation or lifestyle modifications.

In contrast, zero-based budgeting requires you to assign a purpose to every dollar from scratch each month. You build your budget from the ground up, allocating funds based on current needs and priorities rather than historical spending patterns.

Key Differences:

| Traditional Budgeting | Zero-Based Budgeting |

|---|---|

| Uses previous spending as baseline | Starts from zero each period |

| Quick and easy to prepare | Time-intensive but thorough |

| May perpetuate inefficient spending | Forces examination of every expense |

| Backward-looking approach | Forward-looking strategy |

The traditional method offers familiarity and simplicity, making it easily understood and quickly implemented. However, it assumes all current activities and costs are still needed without examining them in detail, potentially carrying forward inefficiencies from previous periods.

Advantages of the 50/30/20 Rule

While the 50/30/20 rule provides a simple framework allocating 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment, zero-based budgeting offers superior flexibility and precision in expense management.

The 50/30/20 rule operates as a broad guideline that may not accommodate individual financial circumstances or varying income levels. Zero-based budgeting, however, ensures optimal resource allocation by requiring you to justify every expense category based on your specific situation and priorities.

Superior Benefits of Zero-Based Budgeting:

- Complete Dollar Accountability: Every dollar receives a specific assignment, maximising efficiency and minimising wastage

- Adaptability to Variable Income: Unlike the rigid percentage-based approach, zero-based budgeting adjusts seamlessly to income fluctuations

- Personalised Allocation: Rather than following predetermined percentages, you allocate funds based on your actual needs and goals

- Enhanced Strategic Planning: The meticulous nature provides a clearer understanding of your financial situation

- Proactive Financial Management: Regular reviews encourage mindful spending habits for long-term success

Zero-based budgeting particularly benefits those with variable incomes, as it adapts to changing financial circumstances rather than forcing adherence to fixed percentages that may not reflect current reality.

Why It Beats Reverse Budgeting and the 60% Solution

Zero-based budgeting surpasses other popular methods by providing comprehensive financial control and intentional resource allocation. Unlike reverse budgeting, which prioritises savings first and allocates remaining funds to expenses, zero-based budgeting ensures every financial category receives deliberate attention.

The method’s strength lies in its proactive approach to financial management. Rather than setting aside a predetermined amount for savings and hoping the remainder covers all expenses, zero-based budgeting requires you to evaluate and justify each expense category, leading to more informed financial decisions.

Why Zero-Based Budgeting Excels:

- Prevents Financial Blind Spots: Unlike methods that focus primarily on savings allocation, zero-based budgeting examines all spending categories

- Maximises Resource Efficiency: By optimising every dollar’s use, it minimises missed opportunities for additional savings or strategic investments

- Encourages Regular Financial Reviews: The monthly rebuild process fosters consistent evaluation of financial priorities

- Develops Questioning Attitude: Forces consideration of whether each expense truly serves your financial goals

This comprehensive approach transforms your money into a strategic tool for achieving financial objectives. Zero-based budgeting’s emphasis on intentional allocation ensures that both immediate needs and long-term goals receive appropriate funding, making it particularly effective for those seeking hands-on financial control and optimisation of every dollar earned.

Real Benefits of Zero-Based Budgeting

Gain Complete Awareness of Your Spending Habits

Zero-based budgeting forces managers to think about how every dollar is spent in every budgeting period, creating an unprecedented level of financial transparency. Unlike traditional budgeting methods that simply modify existing budgets, this approach requires you to justify each expense before adding it to your new budget, even old and recurring expenses.

This comprehensive review process ensures that you consider which areas of your finances are generating value and which expenses may have grown unchecked over time. The method keeps legacy expenses under scrutiny – costs that might not be examined for years in traditional budgeting until there’s some economic shock that forces extreme actions.

By starting from a “zero base” each budgeting period, you develop a deeper understanding of your spending patterns and can identify areas where resources may be misallocated. This level of awareness helps you recognise expenses that tend to grow over time and prevents departments or categories from protecting their budget allocations from necessary cuts.

Adapt Your Budget to Real Life Changes

With zero-based budgeting benefits becoming increasingly apparent, this method offers exceptional flexibility to accommodate life changes and shifting priorities. Since every expense must be justified based on current needs rather than historical spending, your budget can quickly adapt to new circumstances.

The approach enables better alignment with your current strategic goals and priorities. When life situations change – whether it’s a career transition, family growth, or economic shifts – zero-based budgeting allows you to reallocate resources toward areas that will generate the most value in your current situation.

This flexibility prevents you from carrying forward unnecessary expenses from previous periods and ensures your budget reflects your actual needs rather than outdated assumptions. The method’s focus on current justification means you can redirect funds toward emerging priorities without being constrained by past spending patterns.

Prevent Impulsive Spending and Stay Goal-Focused

Zero-based budgeting creates a disciplined framework that naturally discourages impulsive spending by requiring justification for every expenditure. This systematic approach ensures alignment with your strategic goals, as each expense must tie back to your core financial objectives.

The method promotes more disciplined execution by forcing you to consider the added value of each spending decision. Before making any purchase, you must evaluate how it supports your overall financial strategy and whether it deserves priority over other potential uses of those funds.

This enhanced accountability extends throughout your entire budgeting process, creating greater focus on the drivers of your financial success. The requirement to justify expenditures based on key priorities can improve your most important financial areas and help you maintain focus on long-term objectives rather than getting distracted by short-term wants.

The collaborative nature of zero-based budgeting also enhances communication between different areas of your financial life, ensuring all spending decisions support your overarching goals.

Potential Challenges and Solutions

Time Investment Required for Proper Tracking

Zero-based budgeting demands significantly more time and effort compared to traditional budgeting methods. Unlike conventional approaches that simply adjust previous year’s numbers, zero-based budgeting requires building your entire budget from scratch each cycle. This comprehensive approach means evaluating every expense category and justifying each dollar allocated.

The time commitment extends beyond initial setup. Zero-based budgeting isn’t a once-yearly exercise—it requires continuous management on a rolling basis to incorporate updated market data, changing circumstances, and new priorities. You’ll need to regularly review and adjust allocations as situations evolve throughout the year.

Solution: Start by dedicating focused time blocks for budget planning and tracking. Consider investing in proper training to understand the methodology thoroughly. Many people underestimate the learning curve, but viewing this as capability building rather than just a budgeting tool will pay dividends. Remember that while the initial investment is substantial, the enhanced financial control and strategic thinking it develops make the time commitment worthwhile.

Dealing with Variable Expenses Throughout the Year

Variable expenses present one of the most challenging aspects of zero-based budgeting. Unlike fixed costs that remain consistent, variable expenses fluctuate based on usage, seasonal patterns, or unexpected circumstances. Traditional budgeting often handles this through broad estimates, but zero-based budgeting requires more precise planning for these fluctuations.

Common variable expenses include utilities, travel costs, seasonal business expenses, and maintenance needs. These costs can derail your carefully planned budget if not properly anticipated and managed.

Solution: Create detailed expense categories that distinguish between strategic and non-strategic variable costs. For strategic variables—those directly tied to revenue generation or business growth—allocate adequate buffers based on historical patterns and business projections. For non-strategic variables, apply stricter controls and consider if these expenses truly add business value.

Implement rolling forecasts to continuously update your variable expense projections. This approach allows you to redirect funds from underutilised categories to areas requiring additional resources, maintaining the core principle of zero-based budgeting where every dollar has a designated purpose.

Making It Work with Unpredictable Income Streams

Irregular income poses perhaps the greatest challenge for zero-based budgeting implementation. When your income fluctuates significantly month to month, it becomes difficult to assign every dollar a specific job, which is fundamental to this budgeting approach.

Freelancers, commission-based professionals, and seasonal businesses often struggle with this aspect. The temptation is to abandon zero-based budgeting entirely during lean periods, but this undermines the methodology’s effectiveness.

Solution: Build your zero-based budget around your lowest expected monthly income rather than average income. This conservative approach ensures you can meet all essential obligations even during slow periods. Create priority levels for your expenses—essential, important but flexible, and nice-to-have categories.

When income exceeds your base budget, apply the zero-based principle to the additional funds. Rather than loosely spending extra income, deliberately allocate surplus dollars to specific goals such as emergency fund building, debt reduction, or strategic investments. This maintains the investor mindset that zero-based budgeting promotes while accommodating income variability.

Consider implementing a buffer system where you maintain reserves specifically for smoothing income fluctuations, treating this as a strategic investment in financial stability rather than idle money.

Tools and Resources for Zero-Based Budget Success

Best Apps and Software for Zero-Based Budgeting

YNAB (You Need a Budget) stands as the gold standard for zero-based budgeting apps. This platform follows the zero-based budgeting system precisely, requiring users to assign a job to every dollar they earn. When you get paid, you actively decide how much income goes toward spending, savings, and debt. YNAB costs $14.99 monthly or $109 annually, with a 34-day free trial. The app offers bank account syncing, loan payoff simulators, and “YNAB Together” features that allow up to five household members to share one membership.

EveryDollar provides another excellent zero-based budgeting solution, designed by Dave Ramsey’s company. The free version requires manual transaction entry, while the premium version ($79.99 annually or $17.99 monthly) includes automatic bank syncing. Users allocate every dollar of income to specific categories like savings, utilities, and debt, ensuring no unassigned money remains each month.

PocketGuard follows the zero-based budgeting framework by calculating how much money remains after covering bills, debt payments, and savings goals. The app costs $74.99 annually or $12.99 monthly, featuring a “Pace” alert system that warns users if they’re spending their budget too quickly based on remaining funds and days left in the month.

Goodbudget offers a modern twist on envelope budgeting, where monthly income gets allocated into separate “envelopes” for various spending categories. The free version allows manual entry, while Goodbudget Premium ($80 annually or $10 monthly) provides unlimited envelopes and automatic bank syncing.

Using Spreadsheets and Traditional Methods

Now that we’ve covered digital solutions, many users still prefer traditional spreadsheet methods for zero-based budgeting. According to Reddit user feedback analysed in our reference content, Google Sheets and Excel consistently emerge as popular free and customizable alternatives to paid apps.

Spreadsheets offer complete control over your zero-based budget structure, allowing you to create custom categories and formulas that automatically calculate remaining balances after assigning every dollar. You can set up columns for income, fixed expenses, variable expenses, savings goals, and debt payments, ensuring every dollar receives a specific purpose.

The manual approach provides several advantages: no subscription fees, complete data privacy, unlimited customisation options, and the ability to create complex formulas that match your specific financial situation. You can also easily share spreadsheets with household members for collaborative budgeting.

However, spreadsheets require more time investment and lack automatic bank syncing features found in dedicated apps. You’ll need to manually enter all transactions and update balances regularly to maintain accuracy.

Budget Calculators and Templates to Get Started

With traditional methods established, budget calculators and templates provide an excellent starting point for zero-based budgeting newcomers. Many of the apps mentioned offer free trial periods that include access to their built-in calculators and planning tools.

YNAB provides free workshops and educational guides that include template structures for various income levels and family situations. These resources help users understand how to allocate every dollar effectively across essential categories like housing, transportation, groceries, and savings.

EveryDollar includes a “margin finder” feature that acts as a calculator to identify extra breathing room in your budget, along with personalised plans based on your financial situation. The platform offers daily lessons and live group coaching to help users master the zero-based approach.

Free online calculators can help determine optimal allocation percentages for different budget categories. While specific calculator recommendations weren’t detailed in our reference content, the educational resources provided by these major budgeting platforms serve as comprehensive starting points for building your first zero-based budget template.

Zero-based budgeting gives you complete control over your finances by ensuring every dollar has a specific purpose before you spend it. This method helps you stay aware of your spending habits, prevents impulsive purchases, and keeps you focused on your financial goals, whether you’re paying off debt, building an emergency fund, or saving for a major purchase.

While it requires more time and effort than other budgeting approaches, the results speak for themselves—you’ll finally know exactly where your money is going and can make intentional decisions about your financial future.

The key to success with zero-based budgeting lies in consistency and commitment. Track every transaction, create a fresh budget each month, and don’t forget to account for irregular expenses that might derail your plan. Start by listing your income, categorising your expenses in order of priority, and using tools like budgeting apps to streamline the process.

Remember, a zero-based budget doesn’t mean spending every penny—it means giving every dollar a job, whether that’s paying bills, building savings, or enjoying life within your means. Take control of your money today and start building the financial peace you deserve.