Does debt settlement hurt credit score?

Does debt settlement hurt credit score?

You must login to add an answer.

Need An Account, Sign Up Here

Please briefly explain why you feel this question should be reported.

Please briefly explain why you feel this answer should be reported.

Please briefly explain why you feel this user should be reported.

Instagram verification can be a privacy nightmare when you use your personal email. Every account creation links your real identity to Meta’s tracking ecosystem, floods your inbox with promotional emails, and creates permanent data connections you can’t undo. This guide is for social media managers, digital marketers, content creators, and privacy-conscious users who need to […]

Your credit score is tanking and you need results fast. Maybe you’re trying to qualify for a mortgage, get approved for that car loan, or finally move into your dream apartment. Whatever your reason, you’re not alone – millions of Americans struggle with low credit scores that block them from financial opportunities. This guide is […]

The AI gold rush isn’t coming—it’s already here. Right now, thousands of beginners are using simple AI tools to generate serious monthly income, with many breaking the $10K barrier faster than anyone expected. This guide is for complete beginners who want practical, proven strategies to make money with AI in 2026. You don’t need coding […]

SEO success in 2026 demands more than traditional keyword stuffing and link building. You need tools that can navigate AI-powered search engines, track your brand’s visibility in ChatGPT responses, and optimise for Google’s AI Overviews alongside classic organic rankings. This guide is designed for digital marketers, content creators, SEO professionals, and business owners who want […]

In recent years, financial entrepreneur Timur Turlov has attracted attention in the global finance sector as the founder and CEO of Freedom Holding Corp. As financial markets become more interconnected and technology reshapes how investors access global exchanges, companies like Freedom Holding represent a broader shift toward modern, digital-driven financial services. Freedom Holding Corp. operates […]

AI myths are stopping small and medium businesses from tapping into artificial intelligence’s real potential. These misconceptions spread faster than facts, leaving business owners convinced that AI is either too complex, too expensive, or too risky for their operations. This article is for business owners, managers, and decision-makers who want to separate AI reality from […]

Struggling to concentrate at work, during studies, or while tackling daily tasks? We’ve all been there – staring at our computers while our minds wander, or reading the same paragraph three times without absorbing a word. The good news is that small lifestyle changes for better focus can make a dramatic difference in how well […]

Your credit score doesn’t stay the same from month to month, and those monthly credit score changes can feel confusing and stressful. This comprehensive guide breaks down everything you need to know about credit score fluctuations and helps you take control of your financial health. Who this guide is for: Anyone who’s noticed their credit […]

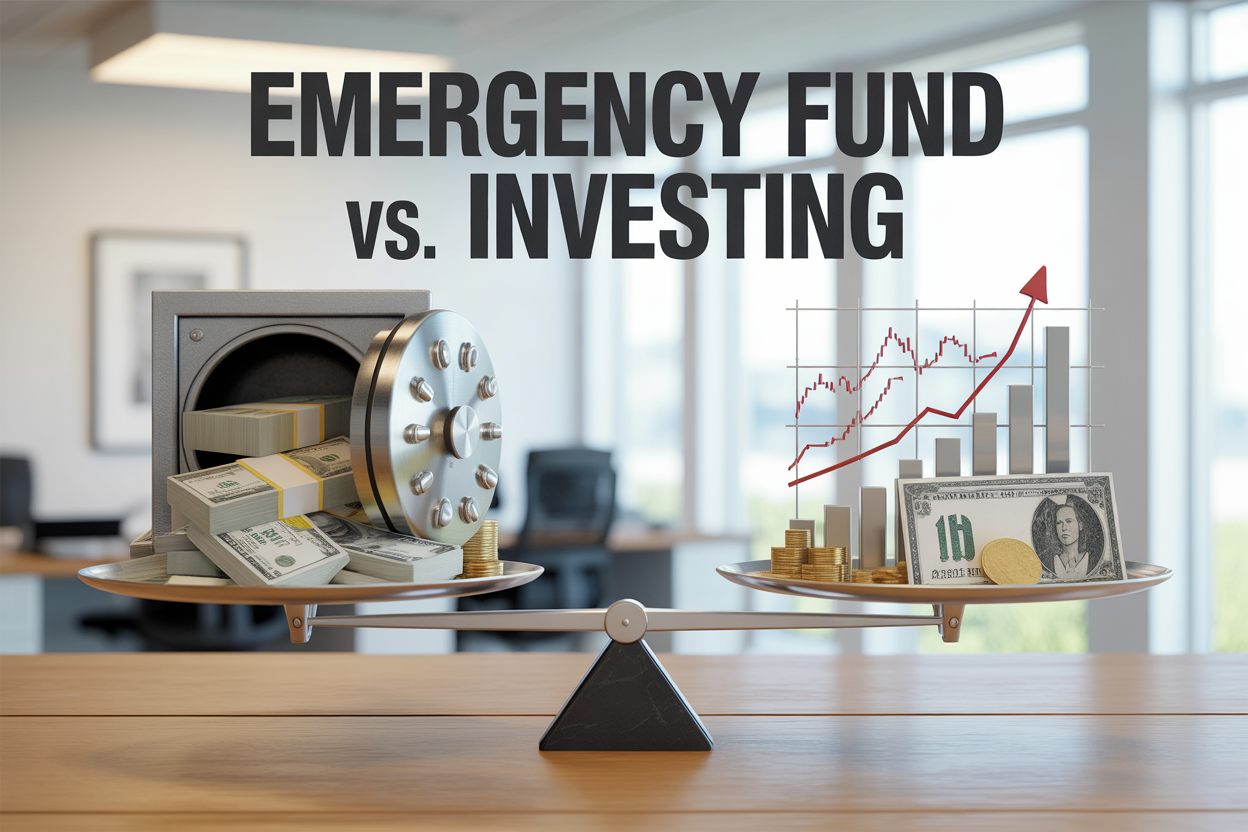

You’ve got money to manage, but you’re stuck on a big question: Should you build an emergency fund or start investing first? This decision stumps many people, especially young adults and new earners who want to grow wealth but also need financial security. You know investing can make your money grow over time, but emergencies […]

Tired of depending on coffee to jumpstart your day? You’re not alone. Many people struggle with low energy in the morning and wonder how to wake up energised without coffee. The good news is that simple, natural morning habits can boost energy levels just as effectively as your daily cup of joe. This guide is […]

Studios charge premium prices for what we can achieve right in our living rooms – and the home yoga benefits often surpass traditional classes. This guide is for busy people who want to start yoga at home, for beginners, experienced practitioners seeking flexibility, and anyone tired of expensive studio memberships that don’t fit their schedule. […]

Technology is advancing faster than ever, and by 2030, several breakthrough innovations will completely change how you live, work, and interact with the world around you. This guide is for tech enthusiasts, business professionals, and anyone curious about the future who wants to understand which emerging technologies will have the biggest impact on daily life. […]

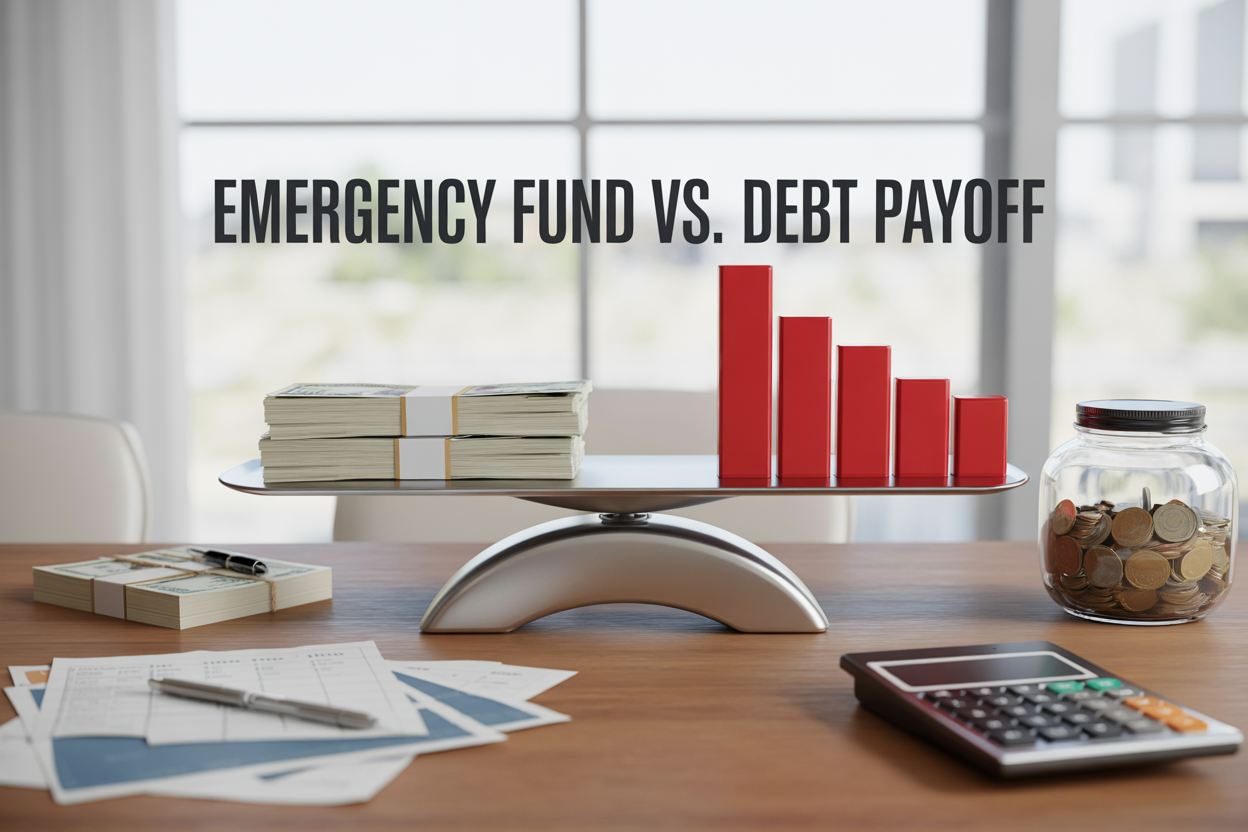

You’re staring at credit card bills and an empty savings account, wondering where to put your next paycheck. The emergency fund vs debt payoff dilemma affects millions of Americans who feel stuck between building financial security and eliminating high-interest debt. This guide is for anyone juggling debt payments while trying to save money—whether you’re recovering […]

Closing old credit cards can tank your credit score in ways most people don’t expect. This guide is for anyone considering cancelling old cards, whether you’re decluttering your wallet or avoiding annual fees. Your credit score takes a hit primarily because closing credit cards affects your credit utilisation ratio. When you lose that available credit […]

AI email assistants have gone from tech novelty to daily necessity, but choosing between Gmail AI vs Outlook AI feels overwhelming when you’re drowning in messages. This guide is for busy professionals, small business owners, and anyone who processes 50+ emails daily and wants to reclaim their time without switching their entire workflow. Smart email […]

Starting a blog feels like launching into uncharted territory. You’re ready to share your expertise with the world, but one wrong move can waste months of effort and hundreds of dollars. This guide is for aspiring bloggers and business owners who want to build a successful blog from day one. We’ll walk through how to […]

Why Audience Understanding is Non-Negotiable Creating content without understanding your audience is like shooting arrows in the dark – you might occasionally hit something, but most efforts miss their mark entirely. Audience understanding forms the bedrock of effective content strategy, transforming generic information into powerful messaging that resonates. When you deeply understand your audience, you […]

How to Choose a Domain When Your Perfect Name Is Taken Finding out your dream domain name taken can feel like a punch to the gut. You’ve brainstormed the perfect name for your business or blog, only to discover someone else got there first. This guide is for entrepreneurs, bloggers, and anyone launching a website […]

A poor credit score can cost you thousands of dollars in higher interest rates and limit your access to loans, apartments, and even some jobs. If you’re dealing with bad credit from past mistakes, preparing for a major purchase, or simply want to improve your financial standing, this 90-day credit improvement plan can help you […]

The 2026 global economic outlook presents a fascinating mix of AI-driven opportunities and traditional recession risks that smart investors need to navigate carefully. This comprehensive analysis is designed for investors, financial advisors, and business leaders in the USA, Canada, and Australia who want to understand how artificial intelligence, shifting monetary policies, and structural market changes […]

Google’s People Also Ask boxes appear in over 43% of search results, yet most marketers ignore this goldmine of SEO opportunities. PAA questions reveal exactly what your audience wants to know, giving you a direct path to featured snippets, voice search optimization, and higher rankings. This guide is for content marketers, SEO specialists, and business […]

Settled a loan and watching your CIBIL score plummet? You’re not alone. Thousands of borrowers face the same challenge after choosing settlement over prolonged EMI struggles, but the good news is that CIBIL score improvement after settlement is absolutely possible with the right approach. This guide is for anyone who has recently settled a loan […]

Your hobby feels more like an escape from work than just a weekend activity. We get it—that creative spark or hands-on satisfaction you find in photography, cooking, woodworking, or whatever gets you excited might actually be pointing toward your next career move. This guide is for anyone tired of watching the clock at their day […]

Small business owners face a growing number of cyber threats that can devastate operations, finances, and reputation. This comprehensive guide is designed for entrepreneurs, small business owners, and team leaders who need practical cybersecurity solutions without breaking the bank or requiring technical expertise. Cybercriminals increasingly target small businesses because they often lack robust security measures. […]

Small business owners and executives are watching remote work reshape their industries in ways that threaten their very survival. While headlines celebrate work-from-home flexibility, a massive economic ecosystem built around office workers is quietly crumbling. This guide is for business leaders, managers, and entrepreneurs who need to understand why remote work is creating unprecedented challenges […]

Your mindset shapes everything—from how you handle setbacks to whether you even try new things. This deep dive is for entrepreneurs, business leaders, and anyone curious about growth mindset vs fixed mindset psychology who wants to understand which approach actually drives success. Many people believe talent and intelligence are set in stone. But research shows […]

Finding Your Perfect Profitable Blogging Niche for 2026: A Strategic Guide Choosing the right blogging niche can make or break your online success. Many new bloggers jump in without research, only to discover their topic has no audience or money-making potential. This guide is for aspiring bloggers, content creators switching niches, and anyone wanting to […]

Most bloggers are leaving serious money on the table by ignoring one of Google’s most visible features. If you’re a content creator, digital marketer, or business owner struggling to increase organic traffic despite publishing consistently, you’re not alone. Over 80% of blogs fail within 18 months, and one major reason is overlooking People Also Ask […]

Making money online in 2026 isn’t about overnight riches or shiny get-rich-quick schemes. The real opportunities exist for people who want sustainable income streams they can actually count on. This guide is for anyone tired of the hype – freelancers looking to diversify their income, professionals wanting to build passive revenue, or entrepreneurs ready to […]

President Trump’s latest threat to impose additional tariffs on India for continuing to import Russian oil has sent ripples through global energy markets. This move targets India’s strategic decision to maintain energy security through discounted Russian crude purchases, despite existing U.S. sanctions and trade pressures. For energy traders, policy analysts, and oil market investors, understanding […]

Immediate Drop: Your credit score will likely decrease by 50 to 100+ points immediately after the settlement is reported. Negative Status: Your credit report will display a "Settled" remark instead of "Closed" or "Paid," which is a red flag for lenders. 7-Year Visibility: This negative entry remainsRead more

-

Immediate Drop: Your credit score will likely decrease by 50 to 100+ points immediately after the settlement is reported.

-

Negative Status: Your credit report will display a “Settled” remark instead of “Closed” or “Paid,” which is a red flag for lenders.

-

7-Year Visibility: This negative entry remains on your credit history for seven years, affecting your future borrowing power.

-

Loan Eligibility: Future loan applications (home, auto, personal) are much more likely to be rejected or approved only at very high interest rates.

-

Better Alternative: Try to negotiate a “One-Time Settlement” where the bank agrees to mark the account as “Closed” (usually by paying the full principal), or look into loan restructuring to avoid the “Settled” tag.

See lessI actually looked into this recently because a friend was considering it for their credit card debt. The reality is that while debt settlement might feel like a huge relief because you're paying less than you owe, it’s quite a blow to your creditworthiness. When you settle, your credit report gets mRead more

I actually looked into this recently because a friend was considering it for their credit card debt. The reality is that while debt settlement might feel like a huge relief because you’re paying less than you owe, it’s quite a blow to your creditworthiness.

See lessWhen you settle, your credit report gets marked with a “Settled” status. In the eyes of Indian lenders, this is a major red flag. Most people assume that once the debt is “gone,” their score will jump back up, but it’s the opposite. Your CIBIL score can drop by 70 to 100 points almost immediately.

The biggest issue is the long-term impact. That “Settled” tag stays on your credit history for about seven years. So, if you plan on applying for a home loan or even a car loan in the next few years, banks will see that you didn’t fulfil your previous obligations.

They might reject your application or charge you a much higher interest rate. If you’re struggling, I’d suggest trying to negotiate a longer repayment period or a lower interest rate first to keep the “Closed” status on your report instead.

Hey! So, the short answer is definitely yes. Think of your credit score like a school report card that shows how well you handle your money. When you do a debt settlement, you are basically telling the bank, "I know I owe you 1 Lakh, but I can only pay 60,000. Can we just call it even?" Even if theRead more

Hey! So, the short answer is definitely yes. Think of your credit score like a school report card that shows how well you handle your money. When you do a debt settlement, you are basically telling the bank, “I know I owe you 1 Lakh, but I can only pay 60,000. Can we just call it even?”

See lessEven if the bank says okay, they don’t just forget about the rest. They report this to credit offices like CIBIL. Instead of your account saying “Paid” or “Closed,” it will say “Settled.” This is like getting a “C” grade instead of an “A.” It tells other banks that you didn’t keep your original promise to pay back the full amount.

This usually makes your score go down quite a bit, and it can stay on your record for several years. It’s always best to try to pay the full amount if you can, so your score stays healthy for when you want a big loan later!

Yes, debt settlement significantly hurts your credit score. When you settle a debt for less than the full balance, lenders report the account as "Settled" to credit bureaus. This indicates you failed to meet your original financial commitment, causing your score to drop by 50 to 100 points or more.Read more

Yes, debt settlement significantly hurts your credit score. When you settle a debt for less than the full balance, lenders report the account as “Settled” to credit bureaus. This indicates you failed to meet your original financial commitment, causing your score to drop by 50 to 100 points or more. The “Settled” status remains on your credit report for seven years, making it difficult to qualify for new loans or credit cards with favourable terms.

See less